S&P 500 – Solid Foundation Amid Positive Economic DataS&P 500 – Solid Foundation Amid Positive Economic Data

The S&P 500 index continues to find support from favorable economic data and a stable macroeconomic outlook for the United States. Despite ongoing challenges, the market reflects optimism fueled by a mix of improving manufacturing indicators, resilient consumer spending, and a potential softening in Federal Reserve policy. Additionally, seasonal trends strongly favor the S&P 500, as December is historically one of the best months for equities.

---

Key Economic Drivers Supporting the S&P 500

1. ISM Manufacturing PMI – Signs of Stabilization

- The **ISM Manufacturing PMI** for November rose to 48.4, beating expectations, although still indicating contraction. This suggests the U.S. manufacturing sector is moving closer to stabilization.

- Input costs showed the slowest inflation in a year, and renewed job creation added to the optimism. Challenges such as weaker international demand and reduced production remain, but improved business confidence is a positive signal.

2. Construction Spending Growth

- Construction spending increased by 0.4% in October, highlighting resilience in the housing and infrastructure sectors. This reflects ongoing consumer and government investment, contributing to economic stability.

3. ISM Manufacturing Prices Paid – Easing Inflationary Pressures

- The ISM Manufacturing Prices Paid index dropped to 50.3, well below forecasts of 55.2. This is a significant development for inflation control, signaling moderating cost pressures within the manufacturing sector.

- Implications:

- Positive for equities: Lower inflation reduces the risk of aggressive Federal Reserve rate hikes.

- Stable monetary outlook: This supports expectations of a gradual shift toward easing monetary policy.

4. Fed Officials’ Support for Gradual Easing

- Recent comments from Fed officials indicate a balanced approach toward monetary policy:

- Christopher Waller highlighted the likelihood of a rate cut in December, citing a balanced labor market and gradual progress on inflation.

- John Williams reaffirmed that inflation is expected to decline toward the 2% target while projecting GDP growth of 2.5% in 2024.

- A potential rate cut could provide a further boost to equities as borrowing costs decrease, encouraging corporate investment.

5. Consumer and Business Optimism

- The S&P Global U.S. Manufacturing PMI pointed to renewed job creation and improving confidence, though challenges such as weaker international demand persist. This mix of cautious optimism and moderating inflation supports steady market sentiment.

---

Seasonality and Market Sentiment

Seasonality is a key supporting factor for the S&P 500 at this time. December has historically been a strong month for equity markets due to holiday-driven consumer spending, portfolio rebalancing, and end-of-year tax considerations. This seasonal strength aligns with the Fear & Greed Index, which currently stands at 64, indicating a **greed-driven sentiment** that tends to favor further market upside.

---

S&P 500 Outlook

The S&P 500 is well-positioned to benefit from these positive economic indicators:

- Lower inflationary pressures reduce the likelihood of aggressive Federal Reserve action, which is supportive of equity markets.

- Steady GDP growth and a resilient labor market provide a strong foundation for corporate earnings.

- Improved manufacturing confidence and spending on infrastructure create additional momentum for sectors like industrials and materials.

- Strong seasonality and a favorable market sentiment further reinforce the potential for continued gains.

While global uncertainties and weaker international demand could weigh on certain sectors, the overall outlook for the S&P 500 remains bullish, with near-term support from seasonal trends, improving economic data, and the potential for a more accommodative Fed policy stance.

US500.F trade ideas

us500 shortus500

short

Please don't be greedy

ENTRY : yellow point

TP : blue lines

SL :

below red line for LONG position

above red line for SHORT position

INSTRUCTIONS:

For risk and money management:

5% of your wallet for LEV X ≤20

And

3% of your wallet for LEV X ≥ 20

Bullish on Emerging markets for next 8YDespite the amount of negative news, the SPX chart shows me something quite different. For the next 6 years, you have to look for buying opportunities in the stock markets and bitcoin, and only later in gold or real estate.

Grinding higherAll four major US stock indices inched into positive territory in early trade this morning. Yesterday, tech stocks led an advance which saw the NASDAQ add around 1% on the day, and the S&P gain 0.2%. The Russell 2000 was effectively unchanged, while the Dow slipped 0.3%. Overall, the recent price action has slowed to a steady grind higher. This follows the explosive rally across all the majors in November, triggered by Trump’s election victory, and led by the domestically-focused, mid-cap Russell 2000. Last month’s rally has seen if not a change in leadership, at least a broadening in the stock market rally. Financials and industrials have benefitted, while sectors viewed as defensive, such as healthcare and consumer staples, have been largely ignored. This gives ammunition to the bullish perspective. It indicates that investors have the confidence to extend their exposure outside of the market-leading tech sector. At the same time, the prevailing bullishness means that investors are currently spurning ‘safe haven’ defensive stocks. The probability of a 25 basis point rate cut from the Fed this month jumped to 72%, up from 60% on Friday. This followed a speech from the Fed’s Christopher Waller who says he favours a rate cut this month. But he also said he was concerned about the recent uptick in inflation. His colleague, John Williams, said that more work has to be done to get inflation back on track towards the Fed’s 2% target. Today there are speeches from Federal Reserve members Adriana Kugler and Austan Goolsbee. There’s also JOLTS Job Openings, the first major labour market data release this week which culminates with Friday’s Non-Farm Payrolls.

S&P500 INDEX (US500): To the New High

S&P500 Index updated the all-time high and violated a significant

daily horizontal resistance based on that.

It opens a potential for a further bullish continuation.

The next goal for buyers will be 6100 level.

❤️Please, support my work with like, thank you!❤️

Elliott Wave View S&P 500 (SPX) Wave 5 in ProgressShort Term Elliott Wave view on SP500 (SPX) suggests rally from 8.5.2024 low is in progress as a 5 waves impulse. Up from 8.5.2024 low, wave 1 ended at 5627.56 high and pullback in wave 2 ended at 5402.62 low. The Index then extends higher in wave 3 ending at 5878.46 high. The next pullback built a zigzag Elliott Wave structure to finish wave 4 at 5696.51 low like the 1 hour chart below shows. Actually, the SPX is trading higher in wave 5 developing an impulse or ending diagonal structure.

Wave 5 rally is in progress with internal subdivision as another impulse. Up from wave 4, wave ((i)) ended at 6017.31 high and wave ((ii)) retracement ended at 5853.01 low. Wave ((iii)) has started and it is trading in wave v of (iii) of ((iii)). Up from wave ((ii)), wave (i) ended at 5908.12 and wave (ii) correction ended at 5855.29. Then the SPX built a nest ending wave i at 5923.51 and wave ii at 5860.56. Wave iii of (iii) finished at 6025.42 and wave iv pullback at 5984.87 low. From here, we are expecting that wave v of (iii) completes soon and the index should see a pullback in 3 swings as wave (iv) before resuming higher in wave (v) of ((iii)). Near term, as far as pivot at 5850.8 low stays intact, expect pullback to find support in 3, 7, or 11 swing for more upside

SPX: Money, Money and Money Supply Note:

These are just my thoughts and opinions and do not constitute advice!!

If you are interested in reading the article I published in 2023 about the US Money Supply and various indicies, you can read it here:

Thanks all and safe trades!

Spx500 1. Understand how the Forex market works, including currency pairs, pips, and leverage.

2. Develop a clear trading plan with specific entry, exit, and risk management rules.

3. Always use stop-loss orders to protect your capital and limit losses.

4. Risk only 1-2% of your account per trade to avoid significant losses.

5. Trade with the trend, as it’s often safer than going against the market.

6. Avoid overtrading; quality trades are better than a high quantity of trades.

7. Use technical and fundamental analysis to make informed trading decisions.

8. Stay updated on global news that can affect currency values, like interest rates and geopolitical events.

9. Keep emotions in check—fear and greed can lead to poor decisions.

10. Continuously learn and adapt your strategy based on market behavior and personal experience.

Perhaps a 'Santa Rally' is just one step away to begin in 2024Stock markets often enjoy a seasonal share boost during the festive period.

It's been two unpredictable year for stock markets after gloomy 2022 but all we are, traders, investors, TradingViewers are hoping for a successful end-of-year boost in the form of a so-called Santa rally.

Shares have much wide, breather and better performance so far in 2024, amid trade and geopolitical tensions, high inflation and high interest rate.

So... while children are compiling their Christmas lists, traders also want some sweet candies.

Traditionally, festive cheer and holiday household spending make the markets more optimistic during the holiday season, boosting investor portfolios.

But will 2024 follow the trend?

The "Santa rally", a term coined in 1972 by Yale Hirsch, the founder of the Stock Trader’s Almanac, "describes a tendency for the stock market to go up by 1% to 2%" over final five trading days of the outgoing year and the first two of the new one, said Forbes Advisor .

This period has "historically" shown higher stock prices in the S&P 500 SP:SPX 79.2% of the time, says Investopedia .

What drives the Santa rally?

Reasons for the Santa rally are vary and one explanation is the cheery "end of year mood" that means investors are in more of a "buying temperament" rather than selling shares, which pushes up stock prices

Will there be a Santa rally this year?

Probably, Yes. September quarter capped off the best 12-months return (+36.36%) for S&P500 Index since the pandemic stock market recovery in 2020, so there are a lot of hopes that stars will align, and momentum in the markets, helped by declining U.S. interest rate, will push prices higher in the run-up to Christmas.

Sure, there is "no guarantee", though. Sometimes it happens. Sometimes it is not.

The odds of a Santa rally may be in your favor, but the "best option" (author's opinion) is to do nothing, remain invested and be "pleasantly surprised" by another strong month by the new year.

The main technical graph for S&P500 Index says that we right now.. already somewhere above to 6'000 points for SPX Index, and just one step to break it out to reach the next one half-a-mile, i.e. 6'500 points by the end of the year.

Just follow the major upside trend, that's been taken earlier this summer. And that is all.

Merry Christmas y'all, TradingViewers! See you in a Happy New 2025 Year! 💖💖

S&P 500 is climbing upwardsS&P 500 is climbing upwards

The market’s move reflects ongoing digestion of mixed US economic data, supportive seasonality, and cautious optimism among investors.

US Economic Data Highlights

Data provided a mixed snapshot of the US economy, contributing to the market’s recent fluctuations:

- **Chicago Fed National Activity Index (Oct):** Fell to -0.40, below the expected -0.2.

- **Dallas Fed Manufacturing Index (Nov):** Came in at -2.7, worse than the forecast of -2.4.

- **New Home Sales (Oct):** Declined to 0.61M, significantly missing expectations of 0.73M.

- **Richmond Fed Manufacturing Index (Nov):** Plunged to -14, below the forecast of -10.

- **Durable Goods Orders (Oct):** Increased by just 0.2%, underperforming the 0.5% forecast.

- **Initial Jobless Claims (Nov 23):** Reported at 213K, slightly better than expected (216K), but still pointing to a resilient labor market.

- **Chicago PMI (Nov):** Dropped to 40.2, well below the anticipated 44, highlighting weakness in manufacturing.

Market Sentiment and Seasonality

Seasonality continues to work in favor of the S&P 500, as historical trends during this period often support equities. The **Fear & Greed Index**, currently at **66 points**, reflects moderate optimism and a "Greed" sentiment, which typically aligns with risk-on behavior in the markets.

Rate Cut Expectations

Markets remain focused on the Federal Reserve’s upcoming meeting on **December 18th**, with a **62,2%% probability** currently priced in for a **25 basis-point rate cut**. Such a move could provide additional support for equities by easing financial conditions, though its long-term impact remains uncertain.

Geopolitical Risks

While market sentiment has improved slightly, risks remain in the background. The ongoing war in Ukraine continues to pose threats to global stability, with potential knock-on effects on energy prices, supply chains, and economic performance.

Long-Term Trend Intact, but Volatility Likely

The S&P 500’s long-term upward trend remains intact, bolstered by supportive seasonality, stable GDP growth, and investor optimism. However, the current environment of mixed economic data and rising policy uncertainty suggests that market volatility could persist in the short term.

Broader Context

27.11 data underscored a steady but moderating US economy, while forward-looking risks remain:

- **Global Economic Outlook:** The S&P Global forecast anticipates global GDP growth of approximately 3% by 2025, with US growth slowing to below 2% next year and China toward 4%.

- **US Policy Risks:** Potential policy shifts under the new administration could elevate inflation pressures and tighten financial conditions, introducing further uncertainty for equity markets.

Implications for S&P 500

Today’s modest gain shows resilience in the face of mixed signals from economic data and global risks. With supportive seasonality and a strong likelihood of a December rate cut, the S&P 500 may find short-term support. However, investors should remain vigilant, as volatility is likely to persist amid policy uncertainties and geopolitical risks.

What’s your outlook for the S&P 500 after today’s rebound? Can the market sustain its gains, or will headwinds from mixed data and global risks take over? Share your thoughts in the comments!

SPX500USD Will Go Up From Support! Buy!

Here is our detailed technical review for SPX500USD.

Time Frame: 1D

Current Trend: Bullish

Sentiment: Oversold (based on 7-period RSI)

Forecast: Bullish

The market is approaching a key horizontal level 6,031.9.

Considering the today's price action, probabilities will be high to see a movement to 6,180.5.

P.S

Please, note that an oversold/overbought condition can last for a long time, and therefore being oversold/overbought doesn't mean a price rally will come soon, or at all.

Like and subscribe and comment my ideas if you enjoy them!

SPX500 Topped Out! You Are Now in a RecessionSPX500 has topped out and has reached the upper trendline of a 100 year trendline that dates back to the 1929 great depression.

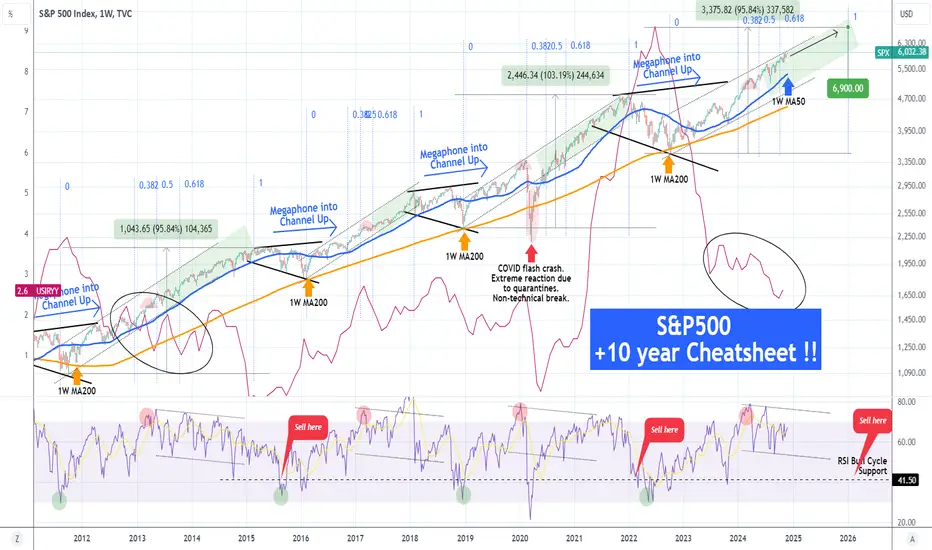

S&P500 This Inflation Cheatsheet shows no correction in 2025.This is a chart we first posted almost 4 months ago (August 14, see chart below) at the time of a CPI date release, where we viewed the S&P500 index (SPX) against Inflation (red trend-line) and calling for an immediate buy:

** The 1W MA50 as the ultimate Support **

Well the price jumped +11% since then from 5440 to over 6000. The first principle of this chart is that as long as the 1W MA50 (blue trend-line) is supporting, investors should stay bullish. This is because all previous multi-year rallies since August 2011 that started within a Channel Up, ended upon a 1W candle close below the 1W MA50 and transitioned into a Megaphone pattern for the new Bear Phase.

** Declining Inflation fueling stocks **

Right now we are still on a declining Inflation trend, very similar to early 2014 (ellipse shape on Inflation), while the 1W RSI of SPX is declining inside a Channel Down. This is a Bearish Divergence, which during all previous SPX Channel Up patterns, didn't make the index top until the RSI broke below its 41.50 Support (notable exception of course the March 2020 COVID flash crash which was a one in 100 years Black Swan event).

** SPX Target and timing **

As a result, while the 1W RSI trades within its Channel Down and above 41.50 and all price candles close above the 1W MA50, we expect the index to extend the multi-year uptrend to 6900, which would represent a +95.84% rise from the October 2022 bottom, similar to the February 2015 High. Notice that the December 2021 top was also of a similar magnitude (+103%).

As far as timing is concerned, we have calculated a model based on the 1W RSI top and the start of its Channel Down. As you see at that point, SPX always makes a medium-term pull-back (red Arc). This tends to be within the 0.382 - 0.618 time Fibonacci levels and on the 2011 - 2014 Bull Cycle, that was within the 0.382 - 0.5 Fib zone. As a result, applying this principle on the current Bull Cycle, the trend is now just 2 months past the 0.618 time Fib and we can expect a Cycle Top around December 2025.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

US 500: Facing a Stern Test in the Week Ahead After closing out the best month of the year so far with a 5.6% gain in November, the US 500 index faces a sterner test in the week ahead. There are several key pieces of tier 1 US economic data and a moderated discussion, which includes the Chairman of the Federal Reserve, Jerome Powell, to consider.

Backdrop for the Week Ahead:

In a sleepy end to last week, the US 500 finished at a new all time closing high of 6038, a move supported by news of Donald Trump's nomination of Wall Street insider Scott Bessent as US Treasury Secretary. This sent US bond yields lower and saw trader expectations increase slightly for another 25bps (0.25%) Federal Reserve interest rate cut at their final meeting of the year on December 18th.

Moving Forward:

Upcoming events in the week ahead may assist the Fed in deciding whether they have room to cut interest rates one more time in 2024, which could help support a Santa rally for the US 500 index into the end of the year.

The ISM Manufacturing PMI is released on Monday at 1500 GMT and the ISM Services PMI is released on Wednesday at 1500 GMT. Service activity has been driving growth in the US economy throughout 2024, so that reading may be more important for traders to consider, depending on whether it continues its recent trend of outperformance.

Then on Thursday evening, Fed Chairman Powell participates in a moderated discussion at 1845 GMT. This may be the final time we get to hear from him before the blackout period for Fed policymakers starts ahead of their rate meeting on December 18th. Any comments he makes on inflation, the economy or the pace of interest rate cuts are likely to impact the US 500.

Finally on Friday, it’s the big event of the week, with the Non-farm Payrolls update for November released at 1330 GMT. The path of the unemployment rate, currently 4.1%, may be an important factor in determining the Fed’s next move, and with it, the direction of the US 500 into the weekend.

Technical Update: Can the Outperformance Continue?

A past failure high is often viewed as a resistance level. When that resistance is marked by the all-time high of an asset, it can take on even more significance.

Are buyers happy to pay the highest price ever and continue to sponsor price strength, or does it again attract sellers, wanting to close longs or even short an asset at historical upside extremes?

Of course, successful closing breaks above a previous all-time high may potentially lead to a more extended rise, depending on developing market conditions. Importantly, last week's move higher in the US 500 ensured a successful closing break above the previous 6030 all-time high posted on November 11th were seen.

While much depends on unknown futures market trends, the question now is, does this suggest there is potential for a continuation of the latest price strength, and if this is the case, where could that resistance be found?

Possible Next US 500 Resistance Levels:

With any asset making new all-time highs, it is effectively in uncharted territory, and it can be hard to gauge where the next resistance points may be. However, within technical analysis, we can use Fibonacci extensions, to highlight potential higher resistance points.

Using the same percentages as Fibonacci retracements (38.2%, and 61.8%) the extent of a previous correction is taken, with 38.2% and 61.8% of that decline projected higher, from the latest peak.

Within the US 500, using the November 11th to November 19th decline (6030 to 5836) and calculating the above percentages, we have found two possible levels to focus on, if the latest break higher does indeed see further strength.

As the chart above shows, the 38.2% extension stands at 6106 and the 61.8% point at 6152, which may mark resistance, if the current strength extends into new higher ground.

Of course, just because Fibonacci extensions have been successful in suggesting higher resistance points in the past, doesn’t guarantee they will do the same this time. However, if these extensions are approached, defense can be watched.

And Possible Supports?

If the latest break to a new all-time high in the US 500 fails to attract fresh buyers and extend current strength, what levels should be watched to the downside as possible supports?

As proved to be the case earlier in November, the rising Bollinger mid-average currently standing at 5950, marks possible support, and closing breaks below this level could lead to a more extended fall in price. If that were the case, the focus may then shift to 5912, which is equal to 38.2% of the November advance.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.

92 Years Resistance S & P 500 PRICE TRADING NEAR MULTI DECADE RESISTANCE . Looks like price try to create a Top

SPX: positive sentiment will holdAnalysts are noting that the S&P 500 ended its best week in 2024. Although the year is slowly approaching the New Year holidays in December, the market sentiment continues to remain quite strong. The index reached its fresh new all time highest level at 6.043, breaking its 6K level.

One of the topics which pushed the semiconductor and chip producers shares to the upside was the Bloomberg report, which noted that additional barriers on the sale of semiconductors to China, imposed by the Biden administration, was not so severe, as the market previously perceived. Market favourite Nvidia surged by 3%, while other semiconductor and chip producers followed the move. Some influence to the equity market came also from the US bonds market, which eased in expectation of further rate cuts and its positive impact to the economy.

As per CME Group FedWatch Tool there is currently 66% odds that the Fed will cut interest rates at their December meeting by additional 25 bps. As long as such a sentiment strongly holds on the market, it could be expected to have a further positive impact on the value of the equity index till its final slowdown nearing the New Year Holiday. At this point, the S&P 500 gained around 24% for the year, which is its best yearly results since 2021.

Nightly $SPX / $SPY Predictions for 12.2.2024🔮

📅Mon Dec 2

⏰10:00am

ISM Manufacturing PMI

📅Tue Dec 3

⏰10:00am

JOLTS Job Openings

📅Wed Dec 4

⏰8:15am

ADP Non-Farm Employment Change

⏰10:00am

ISM Services PMI

⏰10:30am

Crude Oil Inventories

⏰1:45pm

Fed Chair Powell Speaks

📅Thu Dec 5

All Day

OPEC-JMMC Meetings

⏰8:30am

Unemployment Claims

📅Fri Dec 6

⏰8:30am

Average Hourly Earnings m/m

Non-Farm Employment Change

Unemployment Rate

#trading #stock #stockmarket #today #daytrading #swingtrading #charting ⏰

Standard & Poor's: Time is running outIn this idea i will share you the details from an Italian traders that let me think about an important correction from a technical and cyclical point of view:

1) On the max side: We are going to close a 3+ month cycle that could be the final part of the maxi cycle (max side) started at the end of 2021 and now, approaching to a close. Now we are in the third time of the 3+month cycle and we can have just another long try in the zone of the purple trendline (as drown by the zig-zag line), but i don't expect an important raise of the price. Then we can see the test with the trendline and understand better. But surely, max after the first 10 days of december we can start the descendig phase. Yes Sir, no Chrimtas Rally this time.

2) On the min side: We are on the second 3+month cycle, currently counts 18 daily bars and thinkig that we did not found a close for the first half cycle for the first month, and for what we discussed above for the max side cycle close, I expect that the time is running out and we're gonna to find a minimum also because I rember you that we are in 3rd time of the cylce started in Nov 22: first time oct 22, ott 23, second time oct 23, ago 24, third time ago 24 - ???. Then, I remember you that also this cycle, is part of the mega-cycle started after the covid-pandemic in march 2020, and that in this march it turns 5 years. So, I expect that starting shortly, we are going to start a bug desending phase with min target correction 20-25% I expect that the first interesting target from the descending point of view will be in the area of 5,702.86, low of Nov. 4,.

3) Moreover, there is an important divergence between the price and the RSI, an additional sign to support the shift in the market paradigm that I expect.

If u find interesting my idea, please support me with a boost and feel free to ask questions in the comment.

Thanks in advance for the attention.

Hasta la vista!

Omar Lima

SPX near to short term reversalIn my view SPX will reverse @6068 area to target 5650 area where bullish trend will restart to new ATH @6222 where I expect massive crash in 2025 to 4900 at least , in extension we could test 3600 area

Market SnapshotHighly suggest you give it a read

www.elliottwave.com

The socionomic theory of finance (STF) proposes that economic and financial markets are fundamentally different from each other. The differences manifest at both the individual and aggregate levels and arise from the opposing contexts of relative certainty in the economic marketplace vs. pervasive uncertainty in the financial marketplace. In economic markets, producers and consumers, due to knowledge of their own values, consciously apply reason to decision making. This results in exogenously motivated objective pricing. In financial markets, speculators, due to ignorance of others’ future actions, unconsciously apply herding impulses to decision-making. This results in endogenously motivated subjective pricing.

The opposing motivations of producers and consumers cause economic markets to tend toward equilibrium, mean reversion and price stability, in a process regulated at the individual level by utility maximization and at the aggregate level by the laws of supply and demand. The unopposed motivations of speculators cause financial markets to tend toward dynamism in a process regulated at the individual level by spontaneous commands and at the aggregate level by the law of patterned herding. The pricing model for economic markets is the random walk. The pricing model for financial markets is a hierarchical fractal called the Wave Principle, described in the Elliott wave model. Neoclassical economic theory and, in finance, the efficient market hypothesis fail to discern all of these distinctions and inappropriately apply laws of economic causality to finance.

Slowly going up for SPX500USDHi traders,

Last week SPX500USD did not drop but slowly went up some more. It could be making an ending diagonal here.

So next week we could see price go up some more.

Trade idea: Wait for ae correction down to finish and make a change in orderflow to bullish. After that you could trade (short term) longs.

If you want to see more from my analysis, please make sure to follow me, give a like and respectful comment.

This shared post is only my point of view on what could be the next move in this pair based on my analysis. I do not provide trade signals.

Don't be emotional, just trade!

Eduwave

S&P500 Is The Bull Run Over? Short From April 2025Above we can see that the S&P 500 has formed a inverse Head & Shoulder pattern over a 3 year period, before finally breaking this key level of resistance come support 4820.

Usually we expect price to then travel equidistant from the Head to Neckline in the direction of the break. Therefore, we can see that the potential price top after this pattern plays out is 6651.5.

We can also see that the S&P 500 has been trading within a parralel channel, starting with the second half formation of the Head & Shoulder pattern in October 2021, albiet with one false break below the lower trend in September - October 2023 before contiuining to respect the channel until today.

This channel allows us to see where our target of 6651.5 hits out upper channel resistance line. Which happens on the 7th April 2025.

Fundamentally, this coincides with the current landscape being set out by Trump, with his harsh tariffs on Canada, Mexico, Europe and China he is very likely going to cause bottleneck inflation, delayed after he initially implements them in the new year. Combine this with the Federal Reserve lowering interest rates, the yield curve un-inverting, geopolitical risk and energy supply bottlenecks for the AI industry. I believe we are

about to see 5000 hit potentially by the end of 2025.

SPX - 5th wave is unfolding as ending diagonalSharing some upcoming target for spx..

No one can predict the top including me as well.

TA - As a humble science trying to take a guess where top would be