The Utilities Sector The following ETFs are related to the Utilities Sector. The ETFs track different sections of the utilities sector as noted. There are many more ETFs in utilities subsections for the USA and international equities. Included for each ETF are the symbol, the total Assets Under Management (AUM), the Number of Shares in circulation (Shares), the Average daily Trading Volume (Avg Volume) for the 3 months prior to 7/12/2017, the Expense Ratio, and the Bull//Bull type as well as the leverage ratio.

I have tried to copy these data carefully but cannot be held responsible for any mistakes made. These data are important because high volume ETFs are liquid which means you can get in and out quickly and there is a smaller spread between the bid and ask price. This affects the actual profitability of the entry and exits trades. The same considerations applies to put and call options. Use the highest volume ETF that you can.

The risk of the 2x and 3x Leveraged ETFs is that the 2x or 3x ration only applies to one trading day. After that, the ratio declines daily due to the rebalancing effect. NEVER hold 2x or 3x ETFs long term as they fall in value over time. For long shorts (in a non margin account or 401k), just buy the 1x Bear ETF if available. Unfortunately UTLZ is very low volume.

XLU AUM 7.1 Billion, Shares 137.2 M, Avg Volume 11.3 M, Expense Ratio 0.14%, 1x Bull

***Note XLU tracks the Utilities Select Sector Index.

VPU AUM 2.5 Billion, Shares 21.8 M, Avg Volume 145,689, Expense Ratio 0.10%, 1x Bull

***Note VPU tracks the MSCI US Investable Market Utilities 25/50 Index

IDU AUM 754.6 Million, Shares 5.9 M, Avg Volume 81,521, Expense Ratio 0.44%, 1x Bull

***Note IDU tracks the MSCI US Investable Market Utilities 25/50 Index

UPW AUM 14.4 Million, Shares 0.3 Million, Avg Volume 3,252, Expense Ratio, 0.95%, 2x Bull Leveraged

***Note UPW tracks the Dow Jones U.S. Utilities Index

SDP AUM 8.7 Billion, Shares 0.3 M, Avg Volume 3,144 , Expense Ratio 0.95%, 2x Bear Leveraged

***Note SDP tracks the Dow Jones U.S. Utilities Index (-200%)

UTSL AUM 2.5 Million, Shares 0.1 M, Avg Volume n/a, Expense Ratio 1.1%, 3x Bull Leveraged

***Note LOW VOLUME. AVOID

UTLZ AUM 2.3 Million, Shares 0.1 M, Avg Volume 195, Expense Ratio 1.1%, 1x Bear

***Note LOW VOLUME. 1000 shares traded 7/12/17.

XLU

$xlu continuation patterns across the board!-higher time frame showing healthy pullback in defined uptrend finding support at 53.3x area

-mid time frame shows range bound action after a quick downtrend/ signs of accumulation are seen in range bound equilibrium

-momentum is strengthening upward along with volume pressure

-spring candle/pinbar found on mid time frame finding quick support at 53.3x area shows buyers conviction

multiple retests of resistance area 53.6x area shows weakness and high probability of breaking out

lower time frame supports previously mentioned idea with price action making higher lows and higher highs into resistance showing buyers conviction with rising rsi

Long Term Sector RotationSPX vs Major Sectors. I added IBB to cover Biotech.

Please comment. My understanding at this point is to stay in sectors which have good fundamentals and have been relative laggards. The 3 bottom ones at this point seem to be Financials, Technology and XLU / XLP.

Since utilities is a risk-averse sector, so in a pro-growth environment I may want to go with the other 3. XLB is like the coyote / fox from Mickey mouse that runs a few meters off the cliff thinking its still running on solid ground before realizing that there's nothing below it and then falls like a rock. Great if you can time it right.

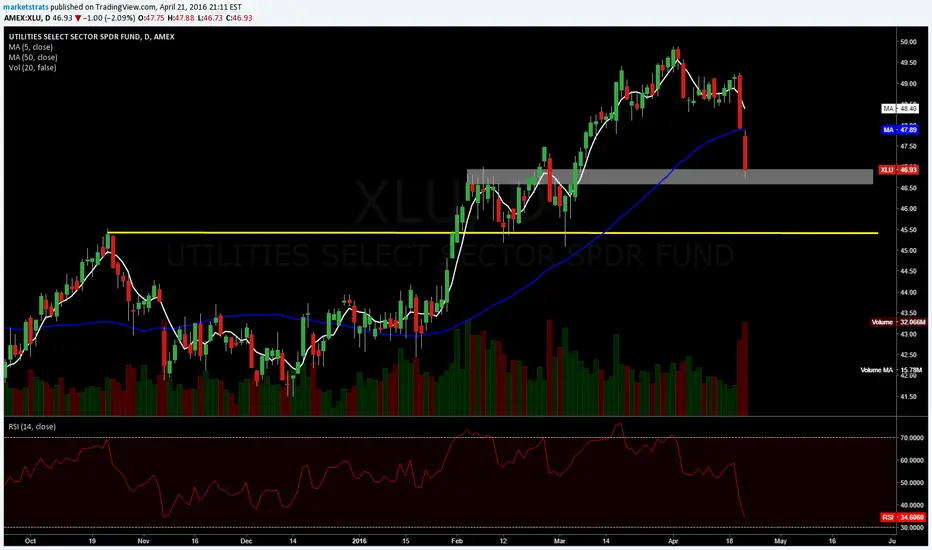

XLU Utilities fund: Waiting for a structural breakdownXLU is a massive, highly liquid fund that only invests in utility companies that are included in the S&P 500. It is one among the cheapest and most liquid options. I am expecting a structural break down. Will only enter if the relative upward strength or the volume of the pair runs out. I have identified the same structure on RSI below. Have a look.

ROLLING: XLU DEC 2ND 45/48.5 SHORT PUT VERT TO DEC 23RDAfter I pulled off the short call of the Dec 2nd iron fly at near worthless today, I rolled the short put side out to the Dec 23rd expiry to give it a little more time to work out, as well to be able to work the call side of the setup effectively. (I have a setup in the Dec 30th expiry already, so didn't want to roll there; Jan was too far out in time for my tastes). I did the roll for a .05 ($5)/contract debit.

Shortly thereafter, I sold a call side against -- the 48/51.50 short call vert short here -- for a .23 ($23)/contract credit, so I'm net credit for the roll. (I could not get enough credit out of the 48.5/52 to bother with, so dropped the spread down a half strike. The resulting setup is pictured here.

Ideally, I need price to move back toward the "body" of the setup to get out for scratch or better. If that doesn't happen, I'll naturally take the call side off at near worthless, and then "lather, rinse, repeat" with the rolling/selling an oppositional side against.

XLU Ranging 17 NOVXLU is ranging around $46-$47 right now and developing a shampoo pattern (head & shoulders) on the 1 Year chart. I sold a straddle and I'll get out as soon as I can.

Each support and resistance has a roughly twin shoulder going back to Feb.

Temporarily neutral to allow the formation to develop.

OPENING: XLU DEC 30TH 42.5/46.5/46.5/49.5 IRON FLYAdding to my core exchange traded fund fly positions here with this high implied volatility rank underlying. (I already have some XLU on, so just adding a "smidgeon" here). The implied volatilty in this isn't great, but then it's almost never "great" ... .

Metrics:

Probability of Profit: 46%

Max Profit: $210/contract

Max Loss: $190/contract

Break Evens: 44.40/48.60

Notes: Will look to manage this like a short straddle -- at 25% max profit ... .

Neutral Long Put Ratios on XLUXLU have a 86% IV Percentile, which means that 86% of the days over the past year the Implied Volatity was below this level.

Custom Put Ratio's

Buy +1 NOV 48 PUT

Sell-2 NOV 47 PUT

BUY +1 NOV 46 PUT

SELL-2 NOV 45 PUT

This will give us a max profit of $171 with a 77% chance of making money. And we only lose if the price goes below $44.64. Since we are adding risk to have better probabilities, if we get assign we would have to buy 200 shares, but it would be 5% below of where we are right now, and since we already have had a 12% down move we can expect a correction soon and we would be able to sell even more premium if we need to.

Defensive sector vs. Cyclical SectorAs long as utilities' performance is weaker against cyclical, we can expect bull market to continue - i.e. expect the ratio (price) to stay inside the channel.

If the ratio (price) breaks the channel above, asset managers are moving more aggressively to defensive stocks, which means that they are anticipating that the economy is slowing significantly - i.e. the bull market to be over. The ratio has been staying higher since the end of the last year, but it has had problems to move out of the channel.

However, daily & weekly Golden Cross is close to happen (50-moving average to cross above 200-moving average), but since June ratio has been making lower lows and lower highs. This is a important ratio to watch. Use this to anticipate overall stock market movement.

OPENING: XLU DEC 2ND 45/48.5/48.5/51 IRON FLYThe underlying implied volatility in XLU is not very high, but it's high relative to where it's been the last 52 weeks (currently, 72 (Dough 52-week implied vol percentile)).

Here are the metrics for the setup:

Probability of Profit: 43%

Max Profit: $175/contract

Max Loss/Buying Power Effect: $175/contract

Break Evens: 46.75/50.25

Notes: As you can see, this isn't a very high probability setup. Basically, it's a risk one to make one. The notion here is to take maximum advantage of the at-the-money premium as you would with a short straddle, which -- like an iron fly -- is a short volatility strategy. If you sell your short options farther away from current price, as you would with an iron condor, your probability of profit increases, but your profit potential decreases because the out of the money strikes bring in less premium.

From a price action standpoint, you're looking for price to stay within your break evens and ideally for volatility to collapse somewhat running toward expiry.

Unlike an iron condor or short strangle, I look to manage at 25% max profit.

TRADE IDEA: XLU NOV 18TH 42/47/47/52 IRON "FLY"I haven't done many of these in the past, but I'm beginning to warm up to them, particular with instruments that wouldn't ordinarily yield jack diddly squat with a traditional iron condor setup.

Here's how this iron fly compares to an iron condor with similar break evens (it would be a Nov 18th 43/46/48/51):*

Probability of Profit: Fly: 52% Condor: 52%

Max Profit: Fly: $220 Condor: $120

Max Loss: Fly: $280 Condor: $180

Break Evens: Same

Theta: Fly: 1.85/day Condor: 1.32/day

Take Profit: Fly: 25% of max ($55 profit) Condor: 50% of max ($60)

Spread "Repair": Same for both setups; roll tested side out for duration and, if feasible, away from current price for strike improvement; sell the oppositional spread against for a credit that exceeds what it cost to roll the tested side. Taking into account all credits received and debits paid, shoot to take off the rolled setup at the original take profit.

As you can see, the probability of profit is the same for setups with the same or substantial similar break evens, and there's little meaningful difference between the profit I would get if I managed the fly like a short straddle (at 25% max) and the condor like a short strangle (at 50% max) ($55 vs. $60).

The research I have looked at for short straddles and short strangles indicates that short straddles reach 25% max in about 30 days on average; short strangles 50% max in about 25 days, www.tastytrade.com (short strangles); tastytradenetwork.squarespace.com (short straddles), which appears to suggest that there is no huge difference in "time to same profit" for the two strategies. (Although those studies involved short straddles and short strangles, you can think of iron flies as "defined risk short straddles" and short strangles as "defined risk short strangles"). Consequently, even though you're receiving greater credit up front for the iron fly, you're probably going to have to wait around for it to reach 25% max profit about the same amount of time as you would an iron fly.

The important takeaway here is that -- but for the iron fly -- I would probably not put on a defined risk trade in XLU. The reward is too small; the risk too great in comparison. So, another tool in the tool box for when you just can't enough credit out of a play in an instrument with your "regular" set of tools ... .

* -- Generally speaking, I would not set up an iron condor this tightly. I'd set up the short option strikes at the edge of the expected move and then the long options out from there 3-5 strikes (e.g., a Nov 18th 42/45/49/52). However, that particular setup would only yield a .72 ($72) credit/contract, and -- were I to manage that trade for 50% of profit -- would only yield .36 ($36) for a setup with a max loss of 2.28/contract ($228). The type of setup for an instrument with these particular metrics (price, implied volatility, etc.) is generally not worth it, in my opinion.

Utilities 8/26/2016Will Utilities volatility spike coincide with stock market volatility spike this time? I think it's worth a bet.

DOW Utilities 7/29/2016It seems if there is no crash in Utilities, then there is no crash in the stock market, we need to watch the lines here. Utilities are very high right now.

Another 61.8 Fib pullback inside the PRZ$XLU continues to range inside the PRZ of a Daily Bat pattern.

Two successful sells I had on this one..

Will the third one be the one that will lead $XLU to its final destination? 45-46$ is my final target zone for this setup

Tomer, The MarketZone

Follow me on TradingView

Subscribe to my newsletters - goo.gl

Follow my blog - goo.gl

Subscribe to my Youtube channel - goo.gl

Bat pattern completed The Bat pattern I've mentioned in the past for $XLU was completed last week.

As you can see there was minor bearish reaction to my harmonic sell zone.

$XLU is very close to 50$ so we may see it try to touch this psychological level.. that's usually what happens.

The bearish scenario for $XLU requires a stop loss above 50.5$ with nice R/R as I aim for 47$ as my first daily target zone and 45$ as secondary

Tomer, The MarketZone

This analysis is part of the Weekly Markets Analysis newsletters

To read more interesting technical reviews for the week goo.gl

To subscribe to the newsletters - goo.gl

Follow my blog - goo.gl

Subscribe to my Youtube channel - goo.gl

Ugly utilities breakdown and continuation on increasing volumeI think we could see 45.50 sooner than later

Utilities (XLU) are toppish, correction expected.The XLU has recentlly reached it's high of early 2015 near $50 which seems to offer strong resistance. A double top seems to be in process. Elliott waves count of 5 waves is completed, a correction seems to have started towards the $46.70/$45.35 area, The wave III should just have started, a fast drop is expected.

RSI (5) and MACD are showing beairhs divergence and the XLU-0.20% is trading far away from its 200 days SMA (at $44.30).

The bond market is also showing a similar exhaustion pattern.

Unapologetically BearishA series of events took place causing me sit back and contemplate market participants (in)sanity. First, it is known that I've was one of the first to stick my neck out and tell it how it is – the U.S. Is facing a recession in 2016 – last April. Soon after, various investment banks flirted with the potential but gave the very realistic situation very low probability of happening.

Needless to say, critics (unfortunately those that “manage” money) have come out to chastise the recession call, which is not backed up hard data but backed subjectively by a rally in equity prices. They repeat the mantra “don't fight the Fed.” Unfortunately, we've already witnessed the carnage bred from the same ignorant complacency as equity markets halve themselves twice in less than 15 years.

Secondarily, last Friday, I watched Mark Zandi, Moody's chief economist, in conjunction with CNBC reporter Steve Liesman, say that the data depicting the sad state of economic affairs was wrong and that we should simply follow the non-farm payroll numbers.

Whoa! This is a classic case of narrative over fact. But, lets look at key economic data points that have already hit cycle highs and rolled over:

Key Data Point Post-Great Recession Peak, YoY %

Non-Farm Payrolls First Quarter, 2015

ISM Non-Manufacturing PMI Third Quarter, 2015

Real Consumption First Quarter, 2015

Agg. Private Sector Wages & Income Fourth Quarter, 2014

Retail Sales and Food Servicess Third Quarter, 2011

Business Sales Second Quarter, 2010

Business Inventory-to-Sales Ratio First Quarter, 2016 (Cycle High)

ISM Manufacturing PMI Fourth Quarter, 2009

Additionally, all is not well in the corporate sector. Last month, market participants saw corporate profits drop 8.4%, nearly 3x more than expected and the third quarter in a row. Furthermore, profits for all of 2015 fell 5.1 percent - the largest drop since 2008. This is much higher then the .6 percent decline the year before.

Mainstream economists don't forecast a looming recession, but when have they ever? Every recession since the early 1980's began with growth above one percent. In 2007, growth expansion was at 1.87 percent, only .13 percent lower than it was in 2015.

When one steps back from market nuances and models for potential of all risks, not only does the picture become more clearer but the ability to adjust when needed becomes more simpler.

In " SPX Pullbacks Are Volumeless, Stay the Course ," I pointed out the lackluster conviction of the equity rally. This still remains the case. Those that "don't fight the Fed" will be sorely disappointed when the only volume swarms in on the elevator drop.

Notice that price action and accumulation on SPY hit a wall and appears to be pealing back:

In April 2015, I issued a 2016 recession call between Q2-Q3 for the U.S. (following my January call for 1,810 on the SPX). After being laughed at, I wonder who will have the last laugh as Atlanta Fed's GDPNow is modeling a mere .4% (with a potential to go negative) for Q1.

At 22.87x trailing 12-months earnings, equities remains extremely expensive and only have been at these levels prior to market crashes, including the market panic of 1893/96, flash crash of 1962, early 1990's recession, the Dot Com bubble and the Great Recession.

Do you feel lucky?

.... I remain unapologetically bearish.

Reiterating my 1,546 SPX target for 2017.

Please feel free to comment and share charts! And follow me @Lemieux_26

Check my posts out at:

bullion.directory

www.investing.com

www.teachingcurrencytr

RIG goes higherI might be a little early here, but I like RIG and I'm BUYING. After a 78.6% retracement off the highs it looks promising. The RSI and %R are oversold and have acted as a good buy spot in the past. The company has positive net income so fundamentally pretty solid. Earnings are a way off so no near term shocks. The 15 min chart shows a double bottom, which usually gives a bounce if only near term . I like $8.97 as a buy point, very low side risk.

XLE Energy SectorWhile its not a done deal, I would be lightening up in the energy sector. I Bearish Bat formation could be forming. Typically they go to 0.886 retracement. We are not there yet, but getting close. Volume is dropping off some. RSI is making a lower high. Look to get back in around $59. I wouldnt try to short this but I wouldn't be going long either. Neutral.

Ether a double top or a historic new high moment for UtilitiesReally? We are really counting on Utilities to lead the market by making a historic new high?