IRRA, Breaking Bullish Trendline TP 1 : > 2740

TP 2 : > 3200

SL : < 1950

Risk In Your Hand

Press Like & Follow if u like my content

--- Thank You ---

Healthcare

NUMI 1000% move potential - are you in?This daily chart is a beauty setup. Just listed today December 16th on the TSX (graduated from the TSXV) and far undervalued compared to its peers.

Bonus facts:

- Health Canada licenses, some exclusive

- Strong influencer on regulatory market

- Multiple successful clinical trials

- NO DEBT - and a warchest full of cash

- Some big acquisitions this year, becoming a corporate umbrella with multiple lines of business

- Awesome Management team

- Well managed financials

Need I say more? Get this gem before everyone else finds out about it. Likely to follow MMED.

$MIRM sniper edition #2*This is not financial advice, so trade at your own risks*

*My team digs deep and finds stocks that are expected to perform well based off multiple confluences*

*Experienced traders understand the uphill battle in timing the market, so instead my team focuses mainly on risk management*

Recap: My team entered $MIRM on October 29, 2021 at $15.70 per share. Our first take profit is at $21.

My team averaged down on our position today at $13.57 per share bringing our share average to $14.63 per share.

Our First Entry: $15.70

Our 2nd Entry: $13.57

First Take Profit: $21

2nd Take Profit: $26

If you want to see more, please like and follow us @SimplyShowMeTheMoney

Buy $ACOR - NRPicks 12 NovAcorda Therapeutics, Inc. a biopharmaceutical company, develops and markets therapies for neurological disorders in the United States. The company markets Ampyra , an oral medication to improve gait in patients with multiple sclerosis (MS).

Buy $SRNE - NRPicks 15 OctSorrento Therapeutics, Inc. is a commercial and clinical-stage biopharmaceutical company developing therapies for cancer, autoimmune, inflammatory, viral and neurodegenerative diseases. It operates through two segments, Sorrento Therapeutics and Scilex.

P&G India BreakoutThe stock has broken out and retested, therefore it may undergo a rally. Trade is supported by brokerage calls and Supports Nearby.

Risk Reward Ratio - 2:1

SL is placed below support zone & Previously upper trendline. The target is placed near swing high.

Note: Market is having weak sentiments, making this a high risk trade. Due Caution Is Required.

long $CMPSLooks like the MACD is still heading down but curling up. RSI is bottoming out as it reaches an important level of support. I think the risk reward at the $28 level is optimal. If you have a high risk tolerance, buy now.

Shrooms are already decriminalized in Denver and are about to be in Detroit.

The TAM which was initially an imaginative number is now becoming real for Compass Pathways. Go long CMPS

www.freep.com

Looks ready to find a floor and launch on the weekly chart.

our beloved $ATOS *This is not financial advice, so trade at your own risks*

*My team digs deep and finds stocks that are expected to perform well based off multiple confluences*

*Experienced traders understand the uphill battle in timing the market, so instead my team focuses mainly on risk management*

$ATOS remains my teams best trade yet, but sadly for you guys this was before we got serious about documenting our trades here at tradingview. Long story short our guys charted and caught an enormous jump from $1.50 to $9+ per share earlier this year.

My team entered $ATOS again today at $2.75 per share and have set our first take profit at $4.

ENTRY: $2.75

TAKE PROFIT 1: $4

TAKE PROFIT 2: $6.50

If you want to see more, please like and follow us @SimplyShowMeTheMoney

Galapagos is it time to buy ? DYOR NFAHealthcare has been getting slapped as of late but there are some fine investment opportunities. Galapagos is one I have been keeping an eye on. It has formed a broadening wedge on the long term and holding nicely on the support line. Fisher on the monthly frame has crossed up and MACD is showing signs of levelling off. LTF, day especially is showing signs of a nice bottom.

PFE to ATH PFE has been following the highs and lows on this bullish run with last bullish run to a T. Some of my most successful plays have been from finding these patterns and trading them. On top of that, the correction on PFE pulled back to the 78 fib line which is very healthy after a big run like it had. I am still very bullish on the next month for PFE and am anticipating new ath next end of month into dec.

TDOC longGood ER, broke above mental resistance $150.00. seems to be forming a base. above $152.45 and i'm seeing $155.77 (VPOC) overall move would be to $185.71.

short term targets are $155.77, $156.92, $158.64, $161.62, $164.24, $171.51 (POC)

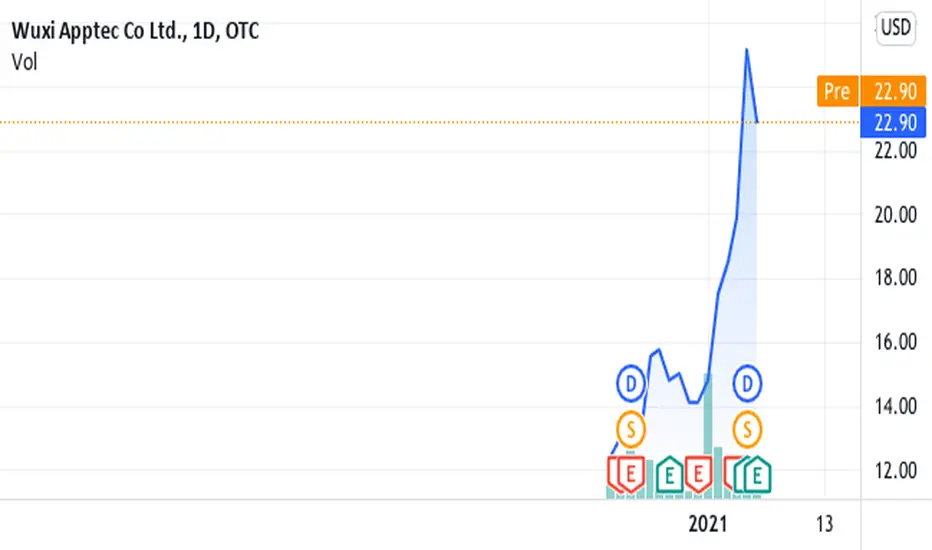

Wuxi Apptec Embraces a More Health-Conscious ChinaAfter a booming year in 2018, Wuxi has yet to slow down. The following article analyzes the success of Wuxi and its shortcomings.

China has released a number of new policies to help make the biopharma industry more transparent and efficient.

By 2020, China had full coverage of medical service systems in rural and urban areas; 90% of residents in China can access the nearest medical point within 15 minutes.

Wuxi Apptec has achieved consecutive quarter-over-quarter revenue growth for 13 quarters since the first beginning of 2018 (other than the first quarter of 2020 due to Covid-19).

Wuxi PharmaTech, a contract research and manufacturing organization, was founded by Dr. Ge Li in 2000. The company changed its name to Wuxi Apptec after Wuxi acquired Apptec Laboratory Services Inc., a US-based medical device and biologics testing company. Wuxi was delisted from the NYSE after going private, with a valuation of USD 3.3 billion. The company has thrived under the leadership of Ge Li as Wuxi went from just 4 people in 2000 to over 28,000 employees in 2021. Ge Li claims that the company's main mission is to provide high-quality research services at a low cost.

Wuxi has been growing rapidly since its inception, but we expect more imminent growth as China rolls out new healthcare-related policies and people become more health-conscious. Although the thriving healthcare market will inevitably attract new entrants that may evolve into strong competitors, Wuxi Apptec is highly likely to withstand the competition.

Rising health awareness

While brands like GNC and The Vitamin Shoppe helped raise healthcare awareness in the west, China was lackluster in this department and put little emphasis on personal well-being. Over the past decade, however, China's healthcare industry grew exponentially as society's attitude towards healthcare took a massive turn. The rising disposable income has led to the paradigm shift from being reactive consumers to proactive consumers. 84% of 3,000 respondents in China, in a survey conducted by Ipsos, reported that they are consciously making health-oriented decisions now.

According to a report by McKinsey, the global wellness economy, accelerated by COVID-19, has an estimated market size of USD 1.5 trillion as of 2021 with 5% to 10% annual growth each year. China reported the highest share of wellness spending online out of the six countries, including Japan. Monosodium glutamate (MSG) is a controversial flavor-enhancing ingredient for its possible adverse effects after consuming more than 3 grams. Major MSG producer Henan Lotus is experiencing a steady decrease in sales as the Chinese population, once the largest consumer of MSG, is becoming more health-aware. Bain and Kantar Worldpanel also reported that sales of chewing gums have also decreased by 14% in the last two years, chocolate sales decreased by 6%, and confectionaries decreased by 4%.

Favorable policies

President Xi announced the initiation of the Health China 2030 (HC 2030) plan in October 2016. The main goals are to prioritize healthcare on a national level, spur innovations in the healthcare industry, promote scientific development, and bring equal access to public health services to all parts of China, especially the country's rural areas. HC 2030 also aims to establish and enhance social policies and institutional systems regarding health, cultivate a healthy environment and intensively promote the advancement of the healthcare industry. Companies in the healthcare industry have seen something of a boost in their revenue as the healthcare trend continues. By 2020, China had extended medical service coverage so thoroughly that 90% of residents could access the nearest medical point within 15 minutes. The medical cost growth was also curbed as 2020 marked the lowest proportion of residents' medical expenditure in 20 years, with 27.7%.

Government policies have favored the development of the healthcare industry in China, especially that of Contract Research Organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs). In 2015, China had a backlog of over 20,000 drug registrations pending review and approval. The National People's Congress (NPC) held a meeting to discuss the reformation of the drug registration system. As a result, China Food and Drug Administration (CFDA) regulators received more resources than in the past, and the government launched the Market Authorization Holder Program (MAH) to make it easier to bring new drugs to the market. Furthermore, the Review and Approve Process (RAP) was simplified and made more efficient. For example, high-quality generics for orphan conditions with robust bioequivalence data will be eligible for expedited review during the CFDA's regulatory process. As of July 2021, a rare disease database (Orphanet) has recognized over 6,000 diseases, propelling pharma companies to roll out more medicine that will undergo a newly implemented process. CROs and CDMOs benefit from these new policies as pharma companies look to increase their research output to develop and produce new drugs. The expedited RAP incentivizes companies to roll out new drugs to cope with the increasing number of orphan diseases recorded.

The unique advantage

Wuxi Apptec is a "fully integrated contract research development and manufacturing organization with the ability to provide one-stop services that offer its clients assistance in discovery, development and manufacturing service demands." The wide variety of services that Wuxi covers allows the company to embrace the soaring healthcare market in China. Wuxi Apptec expects to extend its impact further as the global new drug R&D outsourcing market snowballs. However, Wuxi must persist in its R&D investment to fare well against companies with more flexible cash flow and new entrants with newer technology.

With a boom in customer demand, China's pharmaceutical R&D and manufacturing service market is expected to maintain its current high-speed growth. Wuxi's unique competitive advantage comes from its cost-efficient services. As of 2021, Wuxi has over 28,000 employees, most of whom are chemists, making Wuxi possibly the biggest employer of chemists in the world. Since the company has cheaper labor costs than the industry average, Wuxi can produce almost the same amount of research output for a fraction of the price (around 25% to 40% less than western companies' services).

Additionally, policies such as the MAH, expedited reviews, and HC 2030 have encouraged pharmaceutical innovations in China. Wuxi can capture the rising demand from Chinese pharma companies with its rather high R&D efficiency. Although Wuxi may not have the financial strength of some significant pharma companies with in-house R&D departments, the company will retain its leading position as one of the most profitable R&D and manufacturing businesses in China.

Financial metrics

According to Wuxi's interim report this year, the company realized CNY 10.54 billion total revenue, a year-over-year growth of 45.70%. CNY 2.50 billion came from China, which represents year-over-year growth of 48%. This data showcases the company's ability to capture the rising healthcare tides and demands for research and innovations. 48% growth also marks the largest increase compared to the company's revenue growth in the US and Europe. Wuxi also has a 100% retention rate of its top 10 customers from 2015 to the interim of 2021. As of June 30, 2021, the company's new clients have contributed CNY 849 million in revenue. Frost & Sullivan published a market research report in June 2021, which ranked Wuxi Apptec first by market share in the China-based drug discovery CRO market, pre-clinical and clinical CRO market, and small molecule CDMO market.

Bottom line

The combined forces of new policies and rising healthcare awareness have put Wuxi Apptec in a prime position to consolidate its leadership in China. The company should remain profitable as long as it maintains below industry average labor cost, heavy investment in its R&D department and reasonable M&A strategies to help expand and improve Wuxi's services and operations. Given the recent regulatory crackdown on Chinese tech companies, Wuxi should tread carefully in its effort to capture a more significant share in the Chinese market.

China's rapid growth in the healthcare industry bodes well for the nation, but what does it mean for its people? While the government poured resources into promoting innovations and development in the medical field, the affordability issue gained little attention. Although China has over 90% of residents with basic health insurance plans, it still poses a hefty paycheck for the average worker. Despite the rising wave of healthy living, China has to do more to provide sustainable healthcare.

For the full article with the charts, please visit the original link.

Medtronic & its 100smaThe chart speaks for itself. 100sma has been held and tested multiple times.

RSI has not gone below 35 RSI.

Giving it a little wiggle room makes sense to avoid getting stopped out. The ATR (average true range) is 2 points. So a stop below $127 could potentially provide enough room.

CARE, Swing Trade Upside 15% ??TP 1 : > 500

TP 2 : > 510

SL : < 432

Risk In Your Hand

Press Like & Follow if u like my content

WalgreensI see a possible M pattern forming here. I'm thinking about more people being sick and pharmacy visits over the cold winter season. Walgreens is a great convenience store with solid customer service from my experience. They've been around for a long time. I want to see price retrace the previous high up to 38 - 61%. We are currently in consolidation. However, I believe that since that previous was broken and the current low being higher than the previous, I can see WBA respecting that sentiment on a long term scale. The win goes to the longest holder. On the weekly , we are on the bottom of the Mac D as well and looks to be losing its bearish momentum.

Not advice!

CI- Break out from 5 months downward trendsince 10th May peak, the stock was on bearish trend. As of 6th October is breakout the slope, went back for 1 day but break out again, confirming a trend reversal.

MA50 line is tested and rejected several time in the past 2 weeks but following fibo levels, I believe we look at a climb to 215-220 range before earnings on 4th Nov.

Earnings will define the story onwards

$MRK: Vaccine KrptoniteInvestors should continue to watch Merck and how it plays out here at the 80 level as their COVID drug treatment is pending approval. I believe the market is absolutely sleeping on the significance of this drug and the kind of impact it will have. A treatment is an absolute game changer provided the politics of COVID do not disrupt innovation, transparency and competition in the market. If Merck's drug is effective at treating COVID this will be disastrous to companies like MRNA, JNJ, DVAX, PFE and NVAX. Currently, we're still sitting at less than a 60% fully vaccinated population, the tightest labor supply in history and a work force petitioning vaccine mandates as was witnessed with Boeing workers in Seattle. This will force lawmakers hands to suspend vaccine mandates indefinitely crashing demand for vaccines in the future. The US population has made their stance and vaccine persuasion will only have a diminishing effect from here on out, so the only option is the option that works for everyone in order to minimize division in the country.

$UNH: Think BiggerUnited Healthcare may have posted stellar earnings numbers however that may only be a small fraction of the thesis for this company. If you step back and look at UNH vs SPY using the UNH-SPY pair, there could be a deeper story developing as a new post-COVID era begins.

Insider Activity and a divergence showing.Looking to buy shares Monday and looking at the 1/22 15C options. I expect OSCR to struggle a little to get through 18.5 but when through I expect the mid 20's to trade.

Insider activity: www.tipranks.com

$EVH Merger with Walgreens Will Not Happen Sources SayWe all come here to notice that Walgreens is not interested in the Merger with EVH after digging into the company earnings and realizing there's a conflict of interest in proprietary technology. A Merger makes no sense any more spokesman said. "We'd like to notify private investors today to let them know that the deal doesn't seem to fit our model anymore as far as the health care management software Evolent has to offer" - Walgreens

WACC% 15.48

ROIC -3.73

Operating Margin -4.18

Net Margin -7.28

ROE -11.23

ROA -5.35

3 Year EPS NRI Growth Rate -61.20

Net Income Operations -72.27 70% Worse than 606 companies

Sloan Ratio -42.26

ROCE -4.49

1 Year Asset Growth Rate -7.30

1 Year Debt Growth Rate -21.80

1 Year OCF -881

1 Year Total Growth Rate 8.80

1 Year Revenue Rate Per Share 5.70

MPLNMPLN will need more confirmation of the test for me to become long-term bullish.

Currently 55% bullish 45% bearish

20-9-21 Volume playThree weeks ago insiders started buying and they scheduled a stocks repurchase program.

Check daily for more confirmation.

Logical swing trade opportunity.

$ARKG - Forget Noah, Cathies ARK will keep you afloat! Prime setup for $ARKG as we hit the midway point of Bloody September, the worst month for returns. We've already seen several pullbacks, and with quad witching coming on Sept 17, we're bound to see some volatility.

I fully expect ARKG to fall a little further as the broader market bleeds, but come the quad witching hour, you'll start to see the tides shifting. Growth stocks are looking ready to launch off, and this fund which reflects not only biotech but also AI (as a lot of biotech companies stand to benefit from advancements in AI such as Googles Alpha Fold) is a prime example of the wave count that's prevalent across the board.

Here we have:

1) W2 golden zone target between 80.50-76.79 (green)

2) Leg Y of W2, A = C equal legs target also matches 78.6% retracement of W2 (arrows)

3) Leg C of Y reaching its 14.6-23.6% fib targets between 76.34-75.34 (yellow)

4) Leg Y reaching its 23.6-38.2% fib targets between 77.63-75.70 (red)

5) Large volume profile node peaking around 76.30

This ETF should be in your growth portfolio, and now is the time to get your money ready. Remember, these funds have a 5 year time horizon. Ride the wave!