Buy the dip in TSLA Not a fan of BEVs

But I am more a friend to the truth than to my friends

FSD 12, Optimus, AI

Other OEMs being in the clouds

Growth

My Favorite AI Play - Bandwidth (BAND)Bandwidth (BAND) is my favorite AI play right now.

The chart looks really bad! I get it. Today, it trades for below even its IPO price.

But the reason why I think it's an AI play ready to double, possibly triple, is a fundamental reason that I'll explain in this post.

First of all, let me state something very interesting about Bandwidth - today it's one of the worst performing stocks in the entire market since 2020 and 2021. I don't entirely know why that's the case, but I do think the market has overreacted.

Let me now get the bad news out of the way: when BAND's stock was flying high, management took out several large loans to expand faster and grow globally. Those gains are starting to be realized, but it's key to mention this as the debt profile is still somewhat high. The question now is: can they keep paying it off? They're on target to have little to no debt within the next few years.

Okay, so why is Bandwidth an AI play? To understand this you need to know that Bandwidth is essentially the connector for data that is transmitted over the web. Bandwidth's platform helps data, messages, voice calls, video calls, email, and more travel from Point A to Point B.

For example, when you make a call on Zoom or even Slack or Google Hangouts, it's highly likely your call is being routed over Bandwith's network. The point is, Bandwidth is the toll keeper, the train conductor, for most modern communications that are triggered at scale.

So how does AI fit into this?

That's where this gets good. All of these AI companies NEED a company to help deliver the information to their end consumer. If OpenAI creates a chatbot that works on text message or sends push notifications or can even speak over calls, Bandwidth will most likely be the resource that delivers that information from business to consumer.

What's even more interesting is call centers and the future of talking to call centers to get help or support. In one scenario, you upload all your most frequently asked questions, pair it with an AI service, and then let users call that AI service over the Bandwidth network and now an AI customer support agent is solving issues at scale.

This is just one example.

I could go on and on.

But that's my play!

I own a little Bandwidth and will be watching closely in the coming years.

Supertrend + Hashribbons Showing a Long Term Trend for BTCIn this Video we discuss all the criteria I'm looking at right now for a bitcoin long position.

This includes:

- Hash ribbons smashing all time highs again after looking fairly weak a few days ago.

- Supertrend AI Indicator looking like it's giving a decent trending signal after the last few months of sideways action and traps.

- VWATR Bands expecting a retest/reclaim of the line after losing it(And why).

- And general structure looking a lot better for bitcoin.

Thanks and have a great day :)

Market Meltdown: Wall Street's Shocking Symphony Unveiled!In the heart of financial dynamics, where numbers narrate tales and markets hum a melody, we stand on the cusp of a riveting chapter. The surge in bond yields, the resonance of conflict in Gaza, and the corporate crescendos echo through Wall Street, crafting a narrative that captivates and challenges.

As we step into this unfolding saga, each market movement becomes a note in a symphony—a symphony where every rise in bond yields, every geopolitical tremor, and every corporate revelation plays a crucial role. Join me as we unravel the Overture of Wall Street, decoding the melodies that shape the financial landscape and beckon us into the intriguing world of global finance.

Bond Yields Surge: Unraveling the Threads of Economic Sentiment

The recent surge in the benchmark 10-year U.S. Treasury yield, cresting above 4.9%, serves as a seismic event with far-reaching implications. Traditionally, higher yields spell caution for equity markets, diminishing the allure of stocks in comparison to the safety of fixed-income assets. The market's reaction, characterized by a 1.3% dip in the S&P 500, underscores the anxiety stemming from heightened borrowing costs for both corporations and households.

This surge in bond yields is not merely a statistical blip; it's a harbinger of a delicate dance between the Federal Reserve and the broader economic landscape. The specter of swelling U.S. debt looms large, and as Bloomberg Economics warns, the increase in yields could act as a drag on economic growth, akin to the impact of a Fed rate hike.

Geopolitical Turmoil: A Catalyst for Market Volatility

The geopolitical tableau adds a layer of complexity, with the Gaza conflict acting as a catalyst. The deadly explosion at a Gaza hospital and the subsequent cancellation of a summit with Arab leaders have injected fresh uncertainties into the market psyche. Beyond the tragic human toll, the conflict reverberates through financial markets, notably elevating oil prices.

Oil, the lifeblood of economies, rose nearly 2% to $91.50 a barrel. The Israel-Hamas conflict and optimistic outlooks for Chinese demand became twin engines propelling oil's ascent. Investors, already grappling with bond yield tremors, now face the added challenge of navigating an energy market rife with geopolitical uncertainties.

Corporate Performance: A Tapestry of Triumphs and Tribulations

Against this backdrop, corporate performances play a pivotal role in shaping market trajectories. Morgan Stanley's stock stumbled after reporting a drop in quarterly net income, emblematic of challenges within the financial sector. Simultaneously, Procter & Gamble's shares surged as the company reported a quarterly profit boost, underlining the impact of strategic pricing decisions in an inflationary environment.

The corporate stage is set, with companies wielding the power to either fortify or erode market confidence. In the case of United Airlines, a 7% early decline in shares following a cut in year-end earnings forecasts exemplifies the tightrope walked by companies in a tumultuous market environment.

Market Performance: A Symphony of Red and Green

As the final notes of the market day resonated, the S&P 500, Nasdaq Composite, and Dow Industrials bore the weight of a 1.3%, 1.6%, and 1% decline, respectively. The Russell 2000, reflecting smaller companies, faced a more substantial 2.1% dip. This symphony of red underscores the impact of mixed corporate reports and the tightening grip of rising Treasury yields.

The decline is not confined to domestic shores; the MSCI World index echoes the sentiment, falling in tandem with its U.S. counterparts. The markets, in their collective wisdom, are sending signals of caution, reacting to the interplay of global and domestic variables.

Deciphering the Market's Sonnet

In conclusion, Wall Street's current state is akin to a sonnet, weaving together verses of bond yield surges, geopolitical tumult, and corporate performances. Each stanza contributes to the larger narrative of market sentiment, reflecting the delicate balance between risk and reward. Investors must read between the lines, understanding that every rise in bond yields, every geopolitical tremor, and every corporate report shapes the verses of the market's sonnet.

As we navigate these turbulent waters, an agile and discerning approach is paramount. The future remains unwritten, and while challenges abound, opportunities await those who can decipher the intricate melodies emanating from Wall Street's financial symphony.

Lockheed Martin Corporation (LMT) October 2023 to April 2024

Neutral to Long: The company's fundamentals and dividend history are strong, suggesting a potential long position. However, the recent underperformance (negative YTD return) and the volatility might be a concern, which introduces some caution, hence the neutral stance.

Fundamentals:

Market Cap: $110.91 billion

Operating Margin (TTM): 13.43%

EPS (Earnings Per Share): $27.3

PE Ratio: 16.13

Revenue (TTM): $67.39 billion

Quarterly Revenue Growth YoY: 8.1%

Profit Margin: 10.48%

Return on Equity (TTM): 68.31%

Recent Earnings:

Q3 2023: Estimated EPS was $6.67 (actual EPS not yet reported).

Q2 2023: Estimated EPS was $6.45, and the actual EPS was $6.63, resulting in a positive surprise of 2.79%.

Q1 2023: Estimated EPS was $6.06, and the actual EPS was $6.61, resulting in a positive surprise of 9.08%.

Q4 2022: Estimated EPS was $7.39, and the actual EPS was $7.4, resulting in a slight positive surprise of 0.14%.

Technical Indicators:

5-Year Return: 9.02%

10-Year Return: 16.31%

1-Year Return: 13.94%

YTD Return: -7.52%

Dividend Yield: 2.72%

Volatility (1Y): 21.49%

Sharpe Ratio: 0.7561

Dividends & Splits:

Last Dividend Date: December 29, 2023

Forward Annual Dividend Yield: 2.86%

Forward Annual Dividend Rate: $12.6

Last Split: 2:1 on January 4, 1999

Analysis:

Lockheed Martin has shown consistent growth in its revenue, with a YoY quarterly revenue growth of 8.1%. The company's earnings have been positive, with recent quarters showing a positive surprise in EPS compared to estimates. The company's fundamentals, such as the operating margin and profit margin, are robust. The PE ratio is at a moderate level, indicating that the stock might be reasonably priced. The company has a strong dividend history, which is a positive sign for income-focused investors.

However, the YTD return is negative, indicating some recent underperformance. The volatility is also relatively high, which might be a concern for risk-averse investors.

In conclusion, Lockheed Martin appears to be a fundamentally strong company with consistent growth and a good dividend history. However, potential investors should be cautious about the recent underperformance and consider the company's volatility before making an investment decision.

Please note that this analysis is based on historical data and does not guarantee future performance. Always conduct your own research and consult with a financial advisor before making investment decisions.

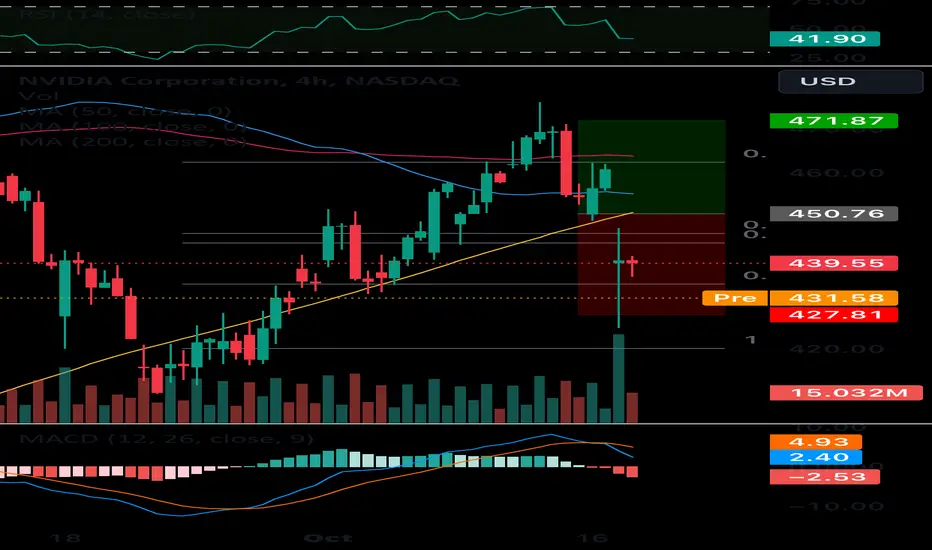

Foxconn and Nvidia are building 'AI factories'Nvidia and Foxconn are working together to build so-called "AI factories," a new class of data centers that promise to provide supercomputing powers to accelerate the development of self-driving cars, autonomous machines and industrial robots.

Nvidia founder and CEO Jensen Huang and Foxconn chairman and CEO Young Liu announced the collaboration at Hon Hai Tech Day in Taiwan on Tuesday. The AI factory is based off an Nvidia GPU computing infrastructure that will be built to process, refine and transform vast amounts of data into valuable AI models and information.

"We're building this entire end-to-end system where on the one hand, you're building this advanced EV car...with an AI brain inside that allows it to interact with drivers and interact with passengers, as well as autonomously drive, complemented by an AI factory that develops a software for this car," said Huang onstage at the event. "This car will go through life experience and collect more data. The data will go to the AI factory, where the AI factory will improve the software and update the entire AI fleet."

The AI factory tie-up builds off a partnership between Nvidia and Foxconn announced in January to develop autonomous vehicle platforms. That agreement involved Foxconn becoming a primary supplier of electronic control units (ECUs) for automakers, which will be built with Nvidia's Drive Orin system-on-a-chip (SoC), a supercomputing AI platform that supports autonomous driving functions. On Tuesday, Foxconn also committed to manufacturing ECUs with Drive Thor, Nvidia's next-gen SoC, after production starts in 2025.

As part of that partnership, Foxconn -- which has been steadily unveiling off-the-shelf EV platforms for automakers to purchase -- said the vehicles it makes as a contract manufacturer will be built with Nvidia's Drive Hyperion 9 platform, which includes not only Drive Thor, but also a suite of sensors like cameras, radar, lidar and ultrasonic that are necessary for self-driving capabilities.

Foxconn is already contracted to build EVs for Fisker, even as it gets sued by its erstwhile partner Lordstown Motors. The automaker will need scale in order to make its AI factories viable, especially if it's going to compete with Tesla.

Pfizer's (PFE) Ulcerative Colitis Pill Etrasimod Gets FDA NodPfizer PFE announced that the FDA has granted approval to its oral, once-daily pill called etrasimod to treat moderately-to-severely active ulcerative colitis (UC). The oral, once-daily, selective sphingosine-1-phosphate (S1P) receptor modulator will be marketed by the brand name of Velsipity (2 mg dose).

The approval for etrasimod was based on data from two pivotal phase III studies, ELEVATE UC 52 and ELEVATE 12. These studies evaluated the safety and efficacy of a daily 2mg dose of oral etrasimod in UC patients who had failed treatment with a JAK inhibitor. Both studies achieved their primary endpoint of clinical remission over placebo and all key secondary endpoints.

An application seeking the approval of etrasimod is also under review in the EU, with a decision from the European Medicines Agency anticipated in first-half 2024.

Velsipity (etrasimod) was added to Pfizer’s inflammation and immunology portfolio with the March 2022 acquisition of Arena Pharmaceuticals.

The oral, once-daily pill for UC, a chronic condition, is an advanced therapy, which, if approved, will offer patients an opportunity to achieve steroid-free remission.

Pfizer’s stock has declined 37.4% so far this year against an increase of 8.5% for the industry.

XAUUSD Bullish trend expected.On Friday, XAUUSD bounced off crucial support at 1820. From now on, we expect the price to be bullish after we retest the 1820 level, with our main target being 1923.

Economic News

The following economic news from last week is relevant to XAUUSD:

US Nonfarm Payrolls: The US economy added 372,000 jobs in August, beating expectations of 300,000. The unemployment rate remained unchanged at 3.5%.

US CPI: US consumer inflation fell to 8.5% in July from 9.1% in June. This was the first time in over a year that inflation had cooled.

US PPI: US producer inflation fell to 8.5% in July from 9.8% in June. This was the first time in over a year that producer inflation had fallen.

Technical Analysis

The strong US jobs data and the cooling of inflation suggest that the US economy is still resilient. This is good news for the dollar, which is likely to remain strong in the near term. However, the fact that inflation is still high means that the Federal Reserve is likely to continue raising interest rates aggressively.

Rising interest rates are typically negative for gold, as they make it more expensive to hold non-yielding assets. However, gold can also benefit from rising interest rates if they lead to fears of a recession.

Based on the current economic news, we expect XAUUSD to retest the 1820 level before moving higher. If the 1820 level holds, we expect the price to continue its bullish momentum towards our main target of 1923.

Entry: 1820

Stop Loss: 1800

Target: 1923

Risk Management

It is important to note that all trading involves risk. The above trading idea is just a suggestion and should not be taken as financial advice. It is important to do your own research and understand the risks involved before placing any trades.

Disclaimer

I am not a financial advisor and this is not financial advice.

S&P 500 FallEarlier in the late summer we predicted S&P 500 drop and this worked out well. This autumn we see futher fall in the S&P 500 through the important psychological level. We see no roots for the US economy to produce more profits while China is openly against it. Military spending cut could be only solution to the problem if this won't happen we see further fall this autumn.

Something big is starting in 2023. Go longThe co-founder of Aptos (APT) says a lot of innovation is coming to the ‘Solana killer’ blockchain project in 2023.

In a new interview with crypto influencer Scott Melker, Aptos CEO and cofounder Mo Shaikh says that the blockchain will see significant development next year, especially catering to decentralized finance (DeFi).

“There’s some really cool DeFi stuff that’s going to be coming live soon that takes advantage of not only things like Move, but also parallel transaction processing. So, you know, central limit order books, AMMs (automated market makers), DEXes (decentralized exchanges) – all of these things will be really cool things to keep an eye on Aptos. That’ll be step changes in innovation relative to everything that we’ve seen in the previous generation of blockchain. So we’re looking forward to all of that.”

The Aptos chain uses a programming language called Move, which was originally created for Diem, Meta’s since abandoned crypto project. Aptos aims to advance Diem’s original goal of creating a fast and scalable blockchain.

Shaikh also says that Aptos was built with billions of users in mind, which appeals to larger entities.

“The other thing that we were focused on was, well, it was kind of frustrating to hear the large companies talk about Web3, but not really do anything. And partly that was because, ‘well, we’re going to do a little pilot and do some testing here, but we know that this stuff doesn’t really work for millions of people. And so we’re not risking bringing all our users to these layer twos or layer ones.’

Back in our early days of Meta, we were building principally for billions of people. So we had taken that approach to protect three-plus billion users. When we started having conversations with folks like Google and Npixel, which is a triple A gaming studio in Korea that has over 10 million users, those folks saw what Aptos can do for their users and actually innovate inside of their organization.

So all those folks have started building on top of Aptos. Web3 users are building new innovative products on Aptos, things that they could not do on the blockchains that were out before. And large entities and enterprises that were… excited about Web3, but weren’t comfortable are now building on Web3 in a meaningful way, and we’re excited to see all those use cases now come to life and in 2023.”

Massive growth is coming for the bull market and you want to make sure you buy the low price for APT.

Some tokens are in a buying range while a majority of the top 20 tokens are still bearish.

Buy up the liquidity before prices really shoot up.

Current price today is 3.73 and that is very low compared to predicted growth this project has.

The Solana killer APTOS will be in the top 10 during the next bull market.

Aptos is in my top 10 investments.

Been playing with 30DTE $MSFT Options, and I'm cautiously LONGBackground

- Been playing with 30DTE MSFT Options for the last 3 months, and I'm cautiously LONG since buyers always seem to buy at Bollinger Bands ranges rather than let it drop below those ranges, regardless of Earnings, News Cycles, or Open Trading Windows.

Growth Fundamentals

1. MSFT is a major holder in OpenAI pre-public stock

2. OpenAI: Will continue to benefit from first mover advantage at scale + API adoption (now part of many workflows)

3. Azure: Continues to benefit from cloud infrastructure adoption

4. Office: Continues to benefit from increased knowledge worker population

🧠 IMHO this combination is what will help us get to annotation #3. (Consumer hardware and gaming business is probably not going to make a significant difference any time soon.)

Technical Analysis

1. Weekly chart shows lots of support levels between now and 312.

2. Expecting buyers to come support 325 and bring us back to the "triple tap" level.

3. I believe we could also range here for awhile due to macro-uncertainty.

Investment Buy and Hold Potential:

1. Certainly a good pickup for the long haul, as MSFT sells to global markets, and has moats in across several different business solutions.

2. AI and Cloud Infra will continue to bring in revenue.

3. Most people are likely comfortable holding MSFT stock if they get assigned

4. Looking for AMEX:SPY to hit $470 before taking profits

Forecast White WAVE My forecast white wave is a range of days which travels from the top to bottom. As it moves to the top, candles seem to dip and as the wave moves down, candles move up.

I laid a yellow arrow pointing at the top of the white wave.

Every 2 vertical lines comes with a forecast of what’s likely to happen. The greenish ones shows it’s moving up to price value.

The orange top trend is my value line. Bottom orange moves along the candles.

Unveiling Alibaba's Secrets: A Technical Analysis of Its Future NYSE:BABA

Based on the weekly ElliotWaves analysis , BABA is currently in a corrective wave structure. The corrective wave structure is a complex wave pattern that can take many different forms. However, the most common corrective wave structure is a three-wave ABC pattern.

BABA appears to be in the wave B of the corrective wave structure. Wave B is a retracement of wave A.

We can expect to see BABA continue to move higher in the coming weeks . However, it is important to note that wave B retracements can be sharp and volatile, so we may have a final push on the downside, before the long-term uptrend begins.

Therefore, it is important to be cautious when trading BABA during the wave B retracement and a stronger price confirmation is needed.

BABA's RSI is currently at approx. 50, which is neutral territory. This suggests that BABA is neither overbought nor oversold. However, the RSI is trending higher, which suggests that BABA is likely to continue to move higher in the coming weeks.

BABA's MACD is currently above its signal line, which is a bullish signal. This suggests that BABA is likely to continue to move higher in the coming weeks.

Potential Direction of BABA on a Weekly Timeframe

Based on the ElliotWaves, RSI, MACD, and other technical tactics, BABA is likely to continue to move higher in the coming weeks. However, it is important to note that the market is unpredictable and there is always the possibility of a trend reversal. Therefore, it is important to be cautious when trading BABA and to use a stop-loss order to protect your profits.

I hope this post is helpful.

This analysis represents is based on the information at the date it is posted.

This analysis does not represent professional and/or financial advice.

You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other content found on this profile before making any decisions based on such information.

Any feedback is encouraged and appreciated. Thank you and have a nice day!

AAPL Downgraded by KeyBanc: Weak Sales Outlook Raises ConcernsIntroduction:

In a recent development, KeyBanc has downgraded Apple Inc. (AAPL) due to a concerning weak sales outlook. This downgrade has sent shockwaves through the market, prompting traders to reevaluate their positions and consider potential shorting opportunities. In this article, we will delve into the reasons behind the downgrade and discuss why traders should exercise caution when dealing with AAPL.

Understanding the Downgrade:

KeyBanc's downgrade of AAPL stems from their analysis of the company's sales outlook. They have identified certain factors that indicate a potential decline in sales, thereby raising concerns about the stock's future performance. As traders, it is crucial to pay attention to such expert opinions and assess the potential impact on our investment strategies.

Reasons for Weak Sales Outlook:

Several factors contribute to the weak sales outlook for AAPL. KeyBanc highlights the following key concerns:

1. Slowing iPhone Sales: The iPhone has been Apple's flagship product, accounting for a significant portion of its revenue. However, KeyBanc predicts a potential slowdown in iPhone sales due to market saturation and intense competition.

2. Trade Tensions: The ongoing trade tensions between the US and China have the potential to disrupt Apple's supply chain and negatively impact its sales. Any escalation in these tensions could further hamper AAPL's growth prospects.

The Call-to-Action: Consider Shorting AAPL with Caution

Given the weak sales outlook and KeyBanc's downgrade, traders should approach AAPL with caution. While shorting AAPL may present an opportunity for profit, it is essential to consider the following factors:

1. Conduct Thorough Research: Before initiating any short position, conduct comprehensive research to understand the potential risks and rewards associated with shorting AAPL. Analyze the company's financials, market trends, and competitor performance to make informed decisions.

2. Diversify Your Portfolio: Shorting AAPL should be part of a well-diversified investment strategy. Avoid placing all your bets on a single stock, as this can expose you to unnecessary risks. Diversification helps mitigate potential losses in case the market responds differently than anticipated.

3. Monitor Market Sentiment: Keep a close eye on market sentiment and news updates related to AAPL. Any positive developments or changes in the company's outlook can quickly impact stock prices. Be prepared to adjust your trading strategy accordingly.

Conclusion:

KeyBanc's downgrade of AAPL based on the weak sales outlook highlights potential challenges for the company in the near future. While shorting AAPL may offer profit potential, traders should exercise caution and conduct thorough research before making any investment decisions. Diversification and monitoring market sentiment are essential for managing risks effectively. Stay informed and adapt your trading strategy accordingly to navigate the uncertainties surrounding AAPL's future performance.

Global Liquidity and BitcoinNow it is obvious that we are facing a scenario more similar to the second one. And no, this does not mean that CRYPTOCAP:BTC will necessarily fall, but it instead tells us that the wind on the market is blowing in the opposite direction🌬️

And growth, most likely, will be insignificant until the trend of quantitative tapering(QT) from the largest central banks does not change.

💡What I mean by "insignificant" is for example no ATH until the halving or no 100k+ in the first half of 2024. Nevertheless, there will be growth, and it will be more than the classic markets can suggest

CYBIN Cybin is a clinical-stage biopharmaceutical company on a mission to create safe and effective psychedelic-based therapeutics to address the large unmet need for new and innovative treatment options for people who suffer from mental health conditions.

Cybin’s goal of revolutionizing mental healthcare is supported by a network of world-class partners and internationally recognized scientists aimed at progressing proprietary drug discovery platforms, innovative drug delivery systems, and novel formulation approaches and treatment regimens.

Billionaire Steve Cohen Buys 19M Shares Of Cybin Stock For Psychedelics R&D, Blake Mycoskie $100M Pledge.

The considerably large acquisition puts Cybin in the limelight with credibility status in ongoing and future work - see Cybin’s recent acquisition announcement of DMT therapeutics developer Small Pharma DMTTF.

Blake Mycoskie On His $100M Pledge To Psychedelics Research

Following a sound pledge of $100 million for psychedelics research, billionaire Blake Mycoskie has updated on how his funding agenda -representing around 25% of his wealth- will unfold.

Mycoskie says he is planning to “give $5 million a year for the rest of the time, until the $100 million runs out,” a yearly sum that “feels right, because the industry still feels nascent.”

That could change in the presence of “a huge opportunity” or in the need of “a huge campaign push.” Although he understands other donors are waiting for further regulatory and scientific success, his personal standpoint is that those aren’t needed in view of solid works authored by Johns Hopkins and New York University, among others.

Banks Across Europe Pause for Breath after Mammoth Rate Hike RunHello guys, my idea on EURGBP is that we are overall in a uptrend and due to the pause for breath after the mammoth rate hike run the trend might reverse or continue little higher before we expect a reversal to the downside.. trade safe. James ❤

SCHW: One of the worse performers in 2023. Cautiously $LONGMain Idea/Insider "Alpha": Many large tech companies like NASDAQ:GOOG and NASDAQ:META use Schwab as their vendor to manage RSU grants. This makes me think Schwab is a great long-term investment and will continue to have good cash flow, assets under management, etc.

In the idea above, I present a bull case and a bear case. At worse, this will be neutral and you can sell options against your position and/or collect dividends.

In high interest rate environments, usually "banks" do well, and so schwab will benefit from halo effect if we see finance stocks continue to do well over the long-term.

Other data points

This website seems bullish as well:

simplywall.st

REWARDS

Trading at 12.7% below our estimate of its fair value

Earnings are forecast to grow 14.51% per year

Earnings grew by 10.8% over the past year

Pays a reliable dividend of 1.81%

Analysts in good agreement that stock price will rise by 35.2%

RISK ANALYSIS

Significant insider selling over the past 3 months

Kelly Criterion and other common position-sizing methodsWhat is position sizing & why is it important?

Position size refers to the amount of risk - money, contracts, equity, etc. - that a trader uses when entering a position on the financial market.

We assume, for ease, that traders expect a 100% profit or loss as a result of the profit lost.

Common ways to size positions are:

Using a set amount of capital per trade . A trader enters with $100 for example, every time. This means that no matter what the position is, the maximum risk of it will be that set capital.

It is the most straight-forward way to size positions, and it aims at producing linear growth in their portfolio.

Using a set amount of contracts per trade . A trader enters with 1 contract of the given asset per trade. When trading Bitcoin, for example, this would mean 1 contract is equal to 1 Bitcoin.

This approach can be tricky to backtest and analyse, since the contract’s dollar value changes over time. A trade that has been placed at a given time when the dollar price is high may show as a bigger win or loss, and a trade at a time when the dollar price of the contract is less, can be shown as a smaller win or loss.

Percentage of total equity - this method is used by traders who decide to enter with a given percentage of their total equity on each position.

It is commonly used in an attempt to achieve ‘exponential growth’ of the portfolio size.

However, the following fictional scenario will show how luck plays a major role in the outcome of such a sizing method.

Let’s assume that the trader has chosen to enter with 50% of their total capital per position.

This would mean that with an equity of $1000, a trader would enter with $500 the first time.

This could lead to two situations for the first trade:

- The position is profitable, and the total equity now is $1500

- The position is losing, and the total equity now is $500.

When we look at these two cases, we can then go deeper into the trading process, looking at the second and third positions they enter.

If the first trade is losing, and we assume that the second two are winning:

a) 500 * 0.5 = 250 entry, total capital when profitable is 750

b) 750 * 0.5 = 375 entry, total capital when profitable is $1125

On the other hand, If the first trade is winning, and we assume that the second two are winning too:

a) 1500 * 0.5 = 750 entry, total capital when profitable is $2250

b) 2250 * 0.5 = 1125 entry, total capital when profitable is $3375

Let’s recap: The trader enters with 50% of the capital and, based on the outcome of the first trade, even if the following two trades are profitable, the difference between the final equity is:

a) First trade lost: $1125

b) First trade won: $3375

This extreme difference of $2250 comes from the single first trade, and whether it’s profitable or not. This goes to show that luck is extremely important when trading with percentage of equity, since that first trade can go any way.

Traders often do not take into account the luck factor that they need to have to reach exponential growth . This leads to very unrealistic expectations of performance of their trading strategy.

What is the Kelly Criterion?

The percentage of equity strategy, as we saw, is dependent on luck and is very tricky. The Kelly Criterion builds on top of that method, however it takes into account factors of the trader’s strategy and historical performance to create a new way of sizing positions.

This mathematical formula is employed by investors seeking to enhance their capital growth objectives. It presupposes that investors are willing to reinvest their profits and expose them to potential risks in subsequent trades. The primary aim of this formula is to ascertain the optimal allocation of capital for each individual trade.

The Kelly criterion encompasses two pivotal components:

Winning Probability Factor (W) : This factor represents the likelihood of a trade yielding a positive return. In the context of TradingView strategies, this refers to the Percent Profitable.

Win/Loss Ratio (R) : This ratio is calculated by the maximum winning potential divided by the maximum loss potential. It could be taken as the Take Profit / Stop-Loss ratio. It can also be taken as the Largest Winning Trade / Largest Losing Trade ratio from the backtesting tab.

The outcome of this formula furnishes investors with guidance on the proportion of their total capital to allocate to each investment endeavour.

Commonly referred to as the Kelly strategy, Kelly formula, or Kelly bet, the formula can be expressed as follows:

Kelly % = W - (1 - W) / R

Where:

Kelly % = Percent of equity that the trader should put in a single trade

W = Winning Probability Factor

R = Win/Loss Ratio

This Kelly % is the suggested percentage of equity a trader should put into their position, based on this sizing formula. With the change of Winning Probability and Win/Loss ratio, traders are able to re-apply the formula to adjust their position size.

Let’s see an example of this formula.

Let’s assume our Win/Loss Ration (R) is the Ratio Avg Win / Avg Loss from the TradingView backtesting statistics. Let’s say the Win/Loss ratio is 0.965.

Also, let’s assume that the Winning Probability Factor is the Percent Profitable statistics from TradingView’s backtesting window. Let’s assume that it is 70%.

With this data, our Kelly % would be:

Kelly % = 0.7 - (1 - 0.7) / 0.965 = 0.38912 = 38.9%

Therefore, based on this fictional example, the trader should allocate around 38.9% of their equity and not more, in order to have an optimal position size according to the Kelly Criterion.

The Kelly formula, in essence, aims to answer the question of “What percent of my equity should I use in a trade, so that it will be optimal”. While any method it is not perfect, it is widely used in the industry as a way to more accurately size positions that use percent of equity for entries.

Caution disclaimer

Although adherents of the Kelly Criterion may choose to apply the formula in its conventional manner, it is essential to acknowledge the potential downsides associated with allocating an excessively substantial portion of one's portfolio into a solitary asset. In the pursuit of diversification, investors would be prudent to exercise caution when considering investments that surpass 20% of their overall equity, even if the Kelly Criterion advocates a more substantial allocation.

Source about information on Kelly Criterion

www.investopedia.com

Pandemic Champion Zoom will be back!In this work, I will analyze Zoom Video Communications, Inc., a leading company in the cloud communication and collaboration sector, which offers online videoconferencing, chat, telephony, webinars, among other services, for different segments and audiences. My investment thesis is that Zoom is an innovative and profitable company that has the potential to remain a leading video-based unified communications platform well into the future. To support this thesis, I will evaluate the qualitative and quantitative aspects of the company. In the qualitative part, I will describe Zoom's business model and strategy, showing how it differs from its competitors, what are its strengths and weaknesses, the opportunities and threats it faces in the global market. In the quantitative part, I will present Zoom's financial and operational data, demonstrating how it has grown in recent years, and what its projections are for the future, for a well-structured technical analysis based on Wyckoff, structures and volume delta.

_____ _____ _____

Company History

The company emerged in 2011, as a result of the vision of Eric Yuan, a former engineer at Cisco Systems, who recognized the need to create a simpler, reliable, and high-quality communication platform. The company launched its main product, Zoom Meeting, in 2013, and has since been growing rapidly in terms of customers, revenue, and profit. The company went public on the NASDAQ stock exchange in April 2019, with an initial public offering (IPO) of $36 per share. In June 2019, the company became part of the Russell 2000 index, which comprises smaller-cap companies in the United States. In April 2020, the company was promoted to the Russell 1000 index, which includes larger-cap companies in the United States. In august 2020, the company surpassed a market value of $100 billion, becoming one of the most valuable technology companies in the world.

Company's Sector of Operation

The company operates in the software as a service (SaaS) sector, which is a business model that provides information technology solutions over the internet, without the need for customers to install or maintain hardware or software. The SaaS sector is a growing and competitive industry, benefiting from digitization, mobility, and cloud trends. Within the SaaS sector, the company excels in the cloud communication and collaboration (CCaaS) segment, which offers online services to facilitate remote work, distance education, and social interactions. The CCaaS segment is dynamic and innovative, adapting to technological changes and consumer demands. It is also a challenging and regulated segment, facing competition from major market players like Microsoft Teams, Google Meet, Cisco Webex, and Skype.

Diversification and Innovation Strategy

The company's strategy is to diversify and innovate its products and services to meet customer needs and differentiate itself from competitors. The company aims to become an open and flexible platform that integrates various cloud communication and collaboration solutions. Some examples of products and services that the company has launched or acquired in recent years include:

Zoom Phone: a cloud telephony system that allows users to make and receive calls using the same Zoom Meeting application.

Zoom Rooms: an integrated system that transforms any physical space into a virtual meeting room with video, audio, and screen sharing.

Zoom Webinar: an online service that enables users to host virtual events with up to 50,000 participants and 100 speakers.

Zoom Chat: an online service that allows users to exchange instant messages with other Zoom users or external contacts.

OnZoom: an online platform that allows users to create, host, and monetize interactive virtual events, such as classes, shows, workshops.

Kites: a startup specialized in real-time automatic translation for video conferences.

SWOT Analysis

It is an essential tool for evaluating a company to invest in, as it offers a broad and organized view of the company's current situation. It consists of identifying the Strengths, Weaknesses, Opportunities, and threats that affect the company's performance. This is a qualitative analysis and does not replace technical or fundamental analysis.

The company's SWOT analysis is as follows:

Strong points:

Freemium model: Zoom offers a free basic plan that allows up to 100 participants and unlimited sessions of up to 40 minutes, attracting those looking for an affordable and quality solution for online communication. Ease of use: It is known for its simple and intuitive interface, which allows participants to start and join sessions with just a few clicks. The company also offers features such as virtual backgrounds and video retouching to enhance the look and feel of those involved during sessions. Global Usage: The platform has a global presence, with more than 300 million daily session participants and more than 213,000 enterprise customers worldwide. It also supports multiple languages and currencies, meeting the needs of diverse audiences. Financial strength: The company has experienced significant revenue and profit growth in recent years, driven by the high demand for online communication during the COVID-19 pandemic. Zoom's total revenue for fiscal 2023 was $4,393 billion, up 7% year-over-year. Business revenue was US$2.409 billion, an increase of 24% compared to the previous year. Brand name: The solution has become a household name and synonymous with online communication, thanks to its popularity and recognition among consumers. Zoom has also received several awards and recognition for its quality and innovation, such as the Webby Award for Best Mobile App in 2020.

Weak points:

Security issues: The company has faced many security and privacy issues in the past, such as “zoom bombing”, which is the unauthorized invasion of sessions by malicious people who interrupt or share inappropriate content. It has also been criticized for sharing consumer data with third parties without proper consent. They don't offer end-to-end encryption: Despite claiming to offer end-to-end encryption, the platform actually uses a type of encryption that allows the company to access session data if it wants to. This raises concerns about the confidentiality and integrity of participant communications. Zoom Rooms: Zoom rooms are a feature that allows stakeholders to create dedicated physical spaces for online communication using specialized Zoom or partner hardware. However, this feature is expensive and requires an additional monthly subscription, which may limit its adoption among customers.

Opportunities:

Growing demand: Demand for online communication is set to continue to grow in the future as more people embrace remote work and hybrid work models. The company can capitalize on this opportunity by expanding its customer base and offering customized solutions for different industries and needs. Up-selling: It can increase its revenue by encouraging basic plan consumers to upgrade to paid plans, which offer more features and benefits, such as longer sessions, more participants, recording and cloud storage, Zoom Phone and Zoom Rooms. Diversification: The platform can diversify its offer of products and services, exploring new markets and segments, such as health, education, entertainment, and e-commerce. The company can also develop new technologies and features, such as augmented reality, artificial intelligence and machine translation, to improve the user experience and differentiate itself from the competition.

Threats:

Intense competition: The company faces strong competition from other players in the online communication market, such as Microsoft Teams, Google Meet, Cisco Webex, Skype, and Facebook Messenger. These competitors have greater financial, technological and marketing resources than it does and can offer integrated and competitive solutions to customers. Regulatory changes: The platform is subject to various laws and regulations in different countries and regions, which may affect its operations and revenues. For example, it may face restrictions or bans from operating in certain markets due to national security, data privacy or human rights concerns. The company may also face fines or penalties for violating these laws and regulations. Dependence on network infrastructure: The quality and performance of Zoom services depend on the availability and reliability of network infrastructure, such as bandwidth, internet speed and stability. Any interruption or degradation of these factors could negatively impact the user experience and the reputation of the solution.

Final qualitative analysis opinion

ZM benefits from its freemium model, ease of use, global usage, financial strength and brand name. But, it also faces challenges such as security issues, lack of end-to-end encryption, cost of Zoom rooms, intense competition, regulatory changes and dependence on network infrastructure. The company can take advantage of videoconferencing demand growth, up-selling and diversification opportunities to overcome its weaknesses and threats. The platform must invest in improving its security and privacy, innovating its products and services and expanding its presence in new markets and segments. Zoom has the potential to remain one of the leading video-based unified communications solutions in the future.

_____ _____ _____

Fundamental Analysis:

We will introduce fundamental analysis, focusing on the company's financial health and performance. For this, we will use financial data from the second quarter of the fiscal year 2024 (ended on July 31, 2023). The financial indicators we will consider are: EBITDA, CFO, ROE, ROIC, Gross Margin, and Operating Margin.

Description of fundamentals:

Source: Yahoo Finance

The company has good liquidity, as it has a high ratio of liquid assets in relation to liquid liabilities, which indicates a low default rate on its basic obligations and low default rates. Furthermore, the company has a large loss in relation to equity and this further reduces its potential market value.

Source: Yahoo Finance

The company has excellent financial health and strong performance. The company demonstrates high operating profit (EBITDA), good cash generation (CFO), good return on equity (ROE) and invested capital (ROIC), and good gross and operating margins. These results show that the company is efficient, profitable, sustainable, and competitive in the video conferencing and online collaboration market.

Other Fundamentals indicators

We will address other economic indicators that are not as necessary but can be incorporated into our fundamental analysis.

Source: Yahoo Finance

The data in this table shows that the company has a good financial performance, but also faces some problems. For one, Zoom Meeting has a high P/E Ratio, which indicates that investors expect future earnings growth from the company. Zoom Meeting also has a high Enterprise Value, which represents the company's total value in the market. These indicators suggest that Zoom Meeting is a successful and innovative company, offering a high-quality and in-demand communication service. On the other hand, Zoom Meeting has a low P/B Ratio and a low PSR, which indicate that the company is trading at a price well above its book value and sales. This could mean that Zoom Meeting is overvalued or faces strong competition in its industry. Furthermore, Zoom Meeting does not pay dividends to its shareholders, which may discourage some investors looking for a stable and secure income. These indicators propose that Zoom Meeting is a risky and volatile company that depends heavily on market expectations and industry trends.

Final opinion of fundamental analysis

It has significant potential for growth and generating value for shareholders, especially in a scenario of increased demand for digital solutions, but it needs to face the threats mentioned previously in the company's SWOT analysis. .

Technical Analysis

To begin the study, first, we observe that the stock was launched in April 2019, and in January 2020, there was a significant increase, as we can see in the weekly chart. With this, we will divide this technical analysis into three parts. In this chart, we have the presence of three volume profiles. It calculates volume by price level based on the Gaussian curve and is excellent for measuring long-term position buildups, especially in a weekly chart like this.

Analysis of the first profile:

ZM Weekly Chart

Note that, since the IPO process, the stock appreciated by 671.09%, which is quite substantial. Many companies were negatively affected during the pandemic, but this one inadvertently benefited from the COVID-19 pandemic. In this first profile, we see the largest position buildup right at the range of 68.75 to 76.95. You can already see 2 candles of aggression, as shown in the second graph, causing significant drops.

Analysis of the second profile:

ZM Weekly Chart

Observing the second profile, we see a lack of demand from buyers and a position buildup on the selling side, unlike what we observed at the beginning.

Analysis of the third profile:

ZM Daily Chart

Upon examining the last profile, we see that despite the market coming from a downtrend channel, we can observe a drastic increase in volume per price level, which is a characteristic of a position buildup. As we gradually see, the seller has been reducing their position, and furthermore, the stock is in a downtrend channel that if it surpasses 78.50, combining it with the fundamentals, we could potentially have an upward trend.

Macroeconomics and Technical Analysis

Surprisingly, Zoom is not the only one that experienced a drop that significantly devalued its stock. Several companies listed on the Nasdaq Composite, including the Nasdaq Composite itself, suffered from a drop that impacted the United States economy.

E-mini Nasdaq Weekly

This was motivated by high inflation, which reached around 9%, which is indeed a very concerning figure for the US economy. By February, inflation had already reached 7.5%, which was already a very high percentage, as technology companies react poorly to inflation. This explains the poor performance of these stocks.

February table

Source: Tradingview Economic Calendar

These data explain the drop in assets listed on the Nasdaq, but surprisingly, Zoom was affected much more than the other companies. Later, when the price started to increase slightly;

And the year 2022 contributed even further to the devaluation of ZM shares. But as we can see, the asset was already in the process of falling long before:

ZM Daily Chart

There was the beginning of a bearish rally there.

Even if the current data are not so favorable, the deflation process that occurred in the United States, together with the artificial intelligence race, could also be a detail that will greatly help in the ZM valuation process.

September table updated

Source: Tradingview Economic Calendar

September's data clearly reveals a drop in inflation, but with several very significant drops, in addition to some negative points such as the reduction in job creation and economic development. Look at the table below:

Source: Tradingview Economic Calendar

Based on this table, Zoom Communications could have a positive result as the company recorded a drop in inflation in September, implying that the costs of products and services decreased. This can benefit consumers and businesses that use the Zoom Service.

Conclusion

Zoom Video Communications Inc. is a company with good financial and market performance, despite the broad devaluation it suffered in 2021/2022. It demonstrates good fundamental analysis with strong revenue and profit growth, a high net margin, low debt and a good market value.

The company also presents good technical analysis. It is undervalued, having been at an all-time low since its IPO, building a position for a likely long-term upward trend. Although the macroeconomy does not favor the variable income market due to a high interest rate of 5.5% (possible readjustment to 5.75% in September), it can also benefit from the ongoing economic deflation, which should stabilize in the end of 2024.

It also has the potential to recover from the decline it has experienced and stand out in the technology market, especially in the videoconferencing segment, which has been less and less in demand post-pandemic and in times of remote work. Demonstrating its ability to innovate and adapt to changes in the economic and social panorama, offering quality and safe solutions to its customers. Therefore, it is believed that Zoom is a good investment option for those seeking long-term profitability and growth.

I hope you enjoyed this article and found it helpful. Thank you for your attention, and until next time!

TSLA -- shortIt looks to me like TSLA will fail to break through both the VWAP since the July high an the top of the declining short-term trading channel. I expect a decline down towards the bottom of the rising intermediate-term trading channel.

Fundamentally, I think that the weakness in Chinese Yuan and the Chinese economy, as well as the price cuts, increasing EV competition from traditional auto makers, and a potential recession in the US will eat into gross margins and USD revenue growth.

This is a short-term trade, which I will express as a vertical put spread with 3 weeks to expiration. My price target is 230, my stop loss will be a close above the declining trend channel since the July high.

Let's go to the Moon!As the halving for Bitcoin approches in April 2024, I am expecting a fast approach to all time highs around end of Nov-Dec of 2024. Bitcoin remains the #1 Cryptocurrency and will be here for time to come. Using the 2020 Bull and Bust Trend, the Ghost Candles mark the path. I do not believe there will be a 2024 Bitcoin Crash as it is getting harder and harder to get more Bitcoin for your moneys worth as price increases on a rapid pace if people feel FOMO. There is a forbes article "Here’s What Caused Bitcoin’s ‘Extreme’ Price Plunge" and from what I read it was due to a Bitmex outage based on being knocked offline. I believe that Futures price shouldnt matter because if you actually hold your Bitcoin in your wallet, price on for Futures shouldnt matter and when you get liquadated on Bitmex, your Bitcoin only goes from your hand to another persons hand. One persons Loss is anothers Gain. I am also 10,000 Matic Tokens to see if I get lucky on the next bullrun, just as a side bet on the altcoin. Bitcoin should be your number one Cryptocurrency holding. Let's go to the Moon!