Selling CHINA50 into trend of higher highs.CHN50 - 22h expiry - We look to Sell at 13310 (stop at 13445)

Buying pressure from 12917 resulted in prices rejecting the dip.

The current move higher is expected to continue.

Previous resistance located at 13304.

This is negative for short term sentiment and we look to set shorts at good risk/reward levels for a further correction lower.

Preferred trade is to sell into rallies.

Although the anticipated move lower is corrective, it does offer ample risk/reward today.

Our profit targets will be 12920 and 12660

Resistance: 13140 / 13615 / 14200

Support: 12660 / 12075 / 11120

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Signal Centre’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Signal Centre.

China

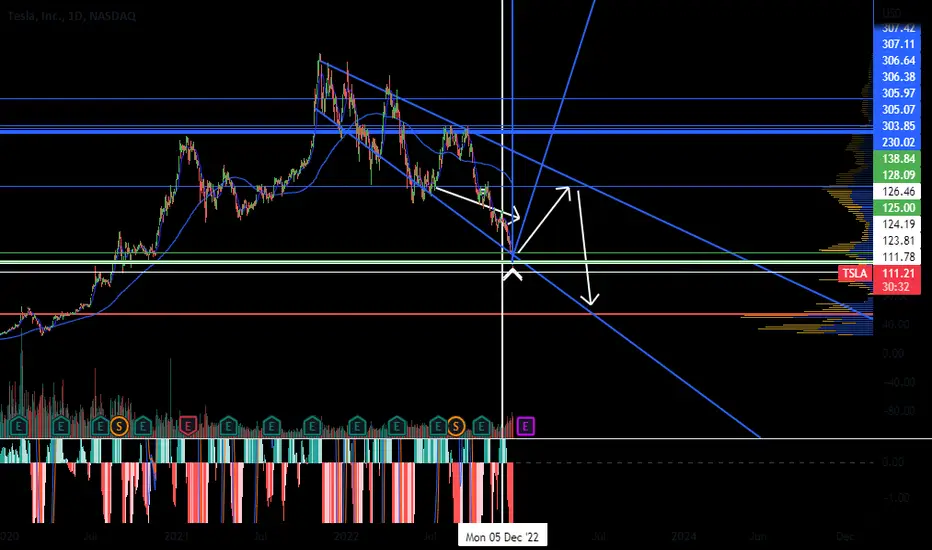

TESLA ChartWe're in for some fun.

Tesla will probably announce the Head of Tesla in the China sector as the NEW CEO of Tesla.

GOLD bullish after news + new supportChina the top gold consumer said the travelers after 8th January would no longer have to go to quarantine.

And as we can see since the open market the gold is on bullish.

We can also watch the support has moved and the channel is making higher highs

However the price coudl retest the 0,5 fibo, so we would put our SL little bit below from the 0,5 line

The Rise and Fall of Chinese YuanCME: USD/Offshore RMB ( CME:CNH1! ), COMEX: Copper Futures ( COMEX:HG1! )

Two weeks ago, China abruptly overhauled its strict Covid policy that had been in place for nearly three years. Lockdowns, health codes, massive testing, and domestic travel restrictions are no longer enforced. “The world changed overnight,” said one of my friends.

From Zero-COVID to “Lying flat”, the literal translation of a Chinese term which means doing the bare minimum to get by, this is a 180-degree policy reversal. It brought overwhelming joy and fear at the same time. People rejoiced over a long-overdue normalization of life and work but feared for surges of widespread Covid infections. I am sending my prayers and hope that a weaker Omicron virus would result in less severe health issues.

China’s reopening could have significant implications to its economy and to financial markets. Today, I focus on its currency, its stock market, and the global commodities markets.

The chart above illustrates how the Chinese Yuan (aka RMB) has moved up and down during the 2-year trade friction and 3-year Covid:

• In 2018, President Trump imposed import duties on thousands of goods originated from China. This sparked a Tariff War that met with retaliation from China.

• As tension escalated and tariffs raised from both sides, the USD/RMB exchange rate depreciated 12%, from 6.28 in March 2018 to 7.16 in December 2019.

• After nearly two years, the two countries signed a First Phase Trade Agreement in January 2020. The Yuan rallied 4% to 6.87.

• Two weeks later, Covid broke out in Wuhan, the capitol city of Hubei Province in central China. It shocked the world. As the pandemic quickly spread all over China and to the rest of the world, RMB depreciated back to 7.16 in May 2020.

• As China’s Zero-Covid policy quickly restored its manufacturing, the “World’s Factory” ramped up exports to other countries which were still shut down by the pandemic. The Yuan rallied again, all the way back to 6.3 by February 2022.

• The citywide lockdown in Shanghai, China’s largest city, was a turning point. Yuan nosedived to a record low of 7.3.

• Finally, the opening of Chinese Communist Party (CCP)’s 20th Congress in October and November signaled a change of courses. With Zero-Covid ending a month after, the Yuan is now back up to around 6.95.

In my view, China’s relations with the West are the key driver of RMB/USD exchange rate. When China embraces the world, Yuan goes up. When it decouples from it, Yuan goes down. As the time of writing, RMB has rebounded 5% in 2 months. I expect Yuan to further appreciate in 2023.

China’s Stock Market

China’s Shanghai Stock Exchange (SSE) index moved sideways. The five-year cumulative return is -7%. This highlighted the severe impacts delivered by both the Trade friction and Covid on the Chinese economy. By comparison, the S&P 500 yields +80% for the first four years. Even after the big selloff in 2022, its 5-year return is +45%.

We are witnessing initial chaos from reopening and Covid surges. After time goes by, I expect China’s stock market to rebound in 2023. For certain, the Chinese economy faces a lot of headwinds. However, massive bailout from the State is on its way. Next year is a year for stock picking. State-run enterprises are in a better position to receive government stimulus disproportionally. My suggestion is to follow the money. Keep an eye on industries and companies which benefit the most from State economic policy.

Commodities Will Get a Lifting

China’s reopening is welcoming news for commodities. Take CME Copper Futures (HG) as an example. Since the past summer, the base metal had been beaten down by 20% amid the market fear of recession. However, it moved above its 50-day MA in November, as the end of CCP’s 20th Party Congress signaled changing courses.

I am also bullish for agricultural commodities. With people going back to work and regaining income, consumption for corn, soybean, wheat, pork, beef, and poultry shall increase next year. This is good news for big exporters such as the US, Brazil, and Argentina.

Takeaways:

1) CME CNH Futures may continue to pull back due to US dollar softening and China reopening. Please note that CNH is quoted RMB per USD. If the Yuan appreciates against the Dollar, futures price would fall. Therefore, if you are bullish on Yuan, shorting CNH is the proper action.

2) SSE stock index may rebound, but we are better off picking individual stocks benefiting from government stimulus. For investors who can’t trade China’s stock market, you could search for Chinese companies listed in Hong Kong, or their American Depository Receipts (ADR) listed in the US markets.

3) Copper (HG) continues to weigh in between demand reduction from global recession and potential demand increase from China’s reopening. In my opinion, recession has already been priced in. The end of Zero-Covid would be an extra booster. Copper could erase its 2022 loss once China factories are pumping out products once again.

I wish everyone a Happy New Year.

Disclaimers

*Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

CME Real-time Market Data help identify trade set-ups and express my market views. If you have futures in your trading portfolio, check out on CME Group data plans in TradingView that suit your trading needs www.tradingview.com

DGSTACC: CN1! MACRO ANALYSIS / CHANNEL CONFIRMATION & SUPPORTIn the chart above we are taking a look at CN1! in the 16 hour timeframe.

1. CN1! reaching an end to pennant formation in vital channel support.

2. Previous pennant breaks in current channel level has been bullish in the past.

3. Important to break past 13300 Supply Ceiling .

4. Channel deviation of 500 points .

5. Channel Above = 13800 - 13300 , Current Channel = 13300 - 12800 , Channel Below = 12800 - 12300.

AUDJPY SHORTDXM : 46% LONG = Still high !!!!!!! Most of retails are still LONG, think in the other side.

Seasonnality : neutral then bull during january but SHORT accordy to the "pattern prediction".

COT Strategy : AUD is reaching a strong resistance around -5 on the COT history Chart AUD.

No FLIP.

Sentiment score :

Daily sentiment : Negative thanks to China covid policy...

Supply/Demande area :

We're on a strong resitance of 89.23.

Support/Resistance :

Strong resistance at 83.23 on DAILY.

Trend :

Under all SMMA = Bearish

Economic News :

*Rapid reopening movements, easing of policy. Are we going to see economic recovery? Morgan Stanley says YES! And raised its 2023 China GDP forecast to 5.4% from 5. But in reality...it's not for today.

*China realizes that opening up is doing too much harm and even though quarantine is no longer mandatory as of January 8, 2023, hospitals, deaths and cases are exploding (not good). There is a good chance they will reverse their decision so this indicates AUD SHORT. If no recovery in China = AUD weak because no or less exports to China since there is less demand.

*Less growth in China means les importation and an impact on the AUD.

The Bank of Japan, in a move that surprises the market, is extending the cap on the control of the 10-year yield curve to 0.50% instead of 0.25% previously. In other words, it is starting to be more hawkish, although it still maintains a strong control. The yen is strengthening and the Nikkei is falling.

YINN | Chinese 3X Bull ETF | LONGThe fund invests at least 80% of its total assets in equity securities of the index and in depositary receipts representing such securities. The index is designed to measure the equity market performance of investable publicly traded "China-based companies" whose primary business or businesses are in the Internet and Internet-related sectors, and are listed outside of Mainland China, as determined by the index provider. The fund is non-diversified.

COVID Zero Softening ? $BABAI'm following $BABA since a while for now and I think that is one of the biggest companies in the sector. China has a lot a potencial but we have to achive some millestones before we breakout this endless falling we're suffering. I'm LONG $BABA from this point. Perhaps until 85$ where the POC developes.

YANG | My Favorite Play | LONGThe fund, under normal circumstances, invests in swap agreements, futures contracts, short positions or other financial instruments that, in combination, provide inverse (opposite) or short leveraged exposure to the index equal to at least 80% of the fund's net assets (plus borrowing for investment purposes). The index consists of the 50 largest and most liquid public Chinese companies currently trading on the Hong Kong Stock Exchange ("SEHK"). The fund is non-diversified.

GREE- BuyGREE stock price has tanked due to the impact from COVID over the last 3 years. It's a perfect time to build a position in your portfolio if you haven't already own this wonderful company.

EPS forecast

2022 - 4.63

2023 - 5.08

2024 - 5.57

Dividend Payout in 2021 = RMB 3 per share. At RMB 30 price per share, that's a 10% dividend yield.

Current valuations are at very attractive levels at around 8 times its earning.

As china reopens from the ending the covid restrictions, I expect GREE to recover smoothly and continue its solid track record.

When the bull market returns I expect the price of Gree to be at 10 to 12 times its earnings.

Stock is currently consolidating at these price levels, I do not see it going lower than its current price due to such an attractive valuation.

Silver - Losing Its Shine?Silver commands value both as a precious metal and an industrial metal. Silver is often considered as a poor man's gold. According to the Silver Institute, Silver is used in solar cells (also known as photovoltaic cells which convert sunlight into electricity), electrical switches, and chemical-producing catalysts. Its unique properties make it nearly impossible to substitute and its uses span a wide range of applications. Every computer, handphone, cars, and appliance contains silver.

Near-term headwinds for photovoltaic manufacturing in China combined with a strong US Dollar are expected to weigh down on Silver prices in the near term. Our short-term outlook for silver is bearish. With a price rally over the past two weeks, we expect prices to retrace in the near term providing a compelling entry for a short position in Silver.

SILVER’S VALUE DRIVERS

Silver has been considered a precious metal for several centuries. However, in the modern economy, silver is valued as both a precious and an industrial metal. Silver’s industrial uses range from electronics, batteries, automobiles, dentistry, and photovoltaics among others. As such, nearly half of the annual worldwide demand for silver was from industrial uses over the past five years. In contrast, only 10%-15% of gold supply is used for industrial purposes.

SILVER’S INDUSTRIAL DEMAND

Photovoltaic demand particularly has been a major factor in recent years with the growing proliferation of solar power. Silver consumption in solar panel production grew 13% in 2021 and accounted for 22% of total industrial usage as per the Silver Institute.

China is the global leader in solar-panel manufacturing accounting for 74% of the module capacity and 85% of the cell capacity in the world according to the IEA. With manufacturing in China remaining muted in the short term due to COVID surge and related lockdowns, photovoltaic production demand over the short term is unlikely to influence Silver prices.

SILVER AS STORE OF VALUE

Silver has underperformed relative to Gold and Platinum this year. Both Silver and Platinum have outperformed over the past month and 3-month periods. Precious metals investments face strong headwinds as investors find relative safety in elevated US Treasury Yields. Although expectations are for the Federal Reserve to ease its rate hiking cycle going forward, that policy pivot remains unlikely anytime soon.

SILVER SUPPLY AND DEMAND BACKDROP

Fuelled by Silver’s price rally in 2020, supply rebounded in 2021 increasing 5% YoY. However, silver supply plunged into a deficit in 2021. This deficit was expected to widen further this year according to the Silver Institute as demand rises (+5%/1030.3 million ounces) was expected to outpace supply (+3%/1,101.8 million ounces).

However, macro backdrop of events this year, from rising inflation, COVID situation in China, to geopolitics, has adversely impacted the demand from the electronics industry leading to excess inventory. Additionally, reduced manufacturing production in China will also lead to lower demand for photovoltaic production. Falling demand, especially in the short term, will likely result in supply outpacing demand.

SILVER TECHNICAL SIGNALS & A PEEK INTO SILVER COT REPORTS

Silver prices rallied over the past two weeks breaching a resistance band ($20.5-$21.32) that has held since July.

Following this rally, RSI moved into overbought territory at 72.18. Additionally, on the 200d and 10d moving average (MA) we see a golden crossover forming. However, if we take a longer short-term MA (20d) to look at the larger uptrend that began on 14th October, the Golden crossover is far from likely to occur.

Moreover, the rally faced resistance at the 200d MA reaching a high of $22.38 which is 3.99% higher than the 200d MA on the day. The highest close was just 2.8% above the moving average on the day. Both these levels are within 2x standard deviation of the Implied Volatility of At the Money Options (31.01%) as seen on CME's QuikVol.

Nevertheless, the current rally does deliver promise as it confidently breached R1 of the pivot point indicator. This level of $20.95 now indicates a support level for the rally.

CME’s Commitment of Traders (COT) tools shows that despite the price increase over the past month, producers have increased the number of short positions from 20.7% to 24.3% on November 15th.

Managed money shorts have decreased from 32.4% to 17.7% while managed money longs have increased marginally from 26.7% to 28.2%.

SHORT SILVER FUTURES TRADE SETUP

CME Micro Silver Futures provide exposure to 1,000 Troy Ounces of Silver with a maintenance margin of $1,700 as of November 22nd. This provides a cost-effective way to get exposure to movements in Silver’s price.

Establishing a short position with an entry price at $21.18/oz with a potential target at $19.88/oz (1x standard deviation of IV of ATM option above the pivot point) by Dec 16th (two days after the next Fed meeting) could provide exposure to a short-term correction in the price of silver yielding 76.47% returns or $1,300. A stop loss at 1x standard deviation of IV of ATM option above 200d MA at $21.88 would protect against an unexpected rally resulting in loss of $700 or -41.18% providing a reward to risk ratio of 1.86. Alternatively, holding the position until the pivot point would lead to 98.82% returns or $1,680.

As the correction is expected to be in the short-term, December futures could provide superior liquidity.

CME’s full-size Silver futures provide exposure to 5,000 Troy Ounces of Silver with a maintenance margin of $8,500 and improved liquidity in case of larger positions.

MARKET DATA

CME Real-time Market Data help identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

DISCLAIMER

Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

This material has been published for general education and circulation only. It does not offer or solicit to buy or sell and does not address specific investment or risk management objectives, financial situation, or particular needs of any person.

Advice should be sought from a financial advisor regarding the suitability of any investment or risk management product before investing or adopting any investment or hedging strategies. Past performance is not indicative of the future performance.

All examples used in this workshop are hypothetical and are used for explanation purposes only. Contents in this material is not investment advice and/or may or may not be the results of actual market experience.

Mint Finance does not endorse or shall not be liable for the content of information provided by third parties. Use of and/or reliance on such information is entirely at the reader’s own risk.

These materials are not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject Mint Finance to any registration or licensing requirement.

Is US Oil Running Low on EnergySUMMARY

Lowered demand projections for Crude Oil as per IEA and OPEC+, softer demand for Crude Oil in China despite partial loosening of restrictions as per EY, the G7-Russian Crude price cap which would lower demand for WTI Crude.

We are short-term bearish on WTI Crude Oil. However, it should be noted that there may be very limited downside in price as the Biden administration plans to replenish the Strategic Petroleum Reserves at prices between $67-$72.

As such, this case study argues that a short position in CME’s NYMEX WTI Crude Oil Futures (February 2023) could provide an interesting trading P&L profile at an entry price of $77.80/barrel with a target of $73.65/barrel with a reward-to-risk ratio of 0.86. A stop loss could be set at $82.61/barrel or the Pivot Point.

OIL PRICE HISTORY

After temporarily dipping at the start of the pandemic, WTI Crude Oil prices rallied through 2021. This was a result of demand bouncing back rapidly as economies re-opened post-pandemic.

This led to dwindling oil reserves in the US and the wider OECD countries. Shortage was further exacerbated by OPEC+ choosing to boost supply gradually.

Finally, prices were pushed even higher given the Russian-Ukraine conflict which threatened to limit the available supply of Crude Oil, of which Russia is the third largest producer according to the IEA.

However, following this peak, prices started to cool off as high inflation dampened demand for oil. This led WTI to erase most of its 2022 gains. WTI prices have retracted back to the start of 2022 twice since then, in September 2022 and in November 2022 again. However, price quickly rebounded off this level as OPEC+ announced supply cuts totaling 2 million barrels per day (real cuts were estimated at 1 million barrels per day as mentioned by Prince Abdulaziz, Saudi Minister of Energy). OPEC+ maintained its lowered output targets at a meeting on the 4th of December 2022.

OPEC also lowered its oil demand forecast for 2022 and 2023 by 100k barrels per day in November.

WTI price has declined 43% from its peak in March.

CHINA

China is experiencing a sharp resurgence in COVID-19 cases this year. Combined with the government’s zero-COVID policy, this led to large scale and strict COVID curbs. This further impacted the demand for oil, of which China is the 2nd largest consumer.

However, at the end of last month, Beijing notably changed its stance and has started to ease restrictions somewhat in parts of the country. Expectations are for China to open in entirety in Spring 2023.

According to EY, demand for Crude Oil in China is expected to be 1.2M barrels per day lower in Q4 2022. This further provides a short-term bearish outlook for crude oil.

STRATEGIC PETROLEUM RESERVE

To better manage spike in oil demand following the pandemic, Biden administration has been drawing large amounts of crude oil from its Strategic Petroleum Reserves. They drew nearly 200 million barrels from the Strategic Petroleum Reserves in 2022. In a mid-term election year, the administration was forced to resort to this to tame sky-high gasoline prices at pumps.

The Biden administration’s move has been seemingly successful in managing the price of gasoline which has declined from $5 to $3.5. Unsurprisingly, this has also drained a large portion of the US strategic reserves, taking it down to 389.1 million barrels, its lowest level since 1984.

The Biden administration has stated intentions to replenish the Strategic Petroleum Reserves when prices are between $67-$72 per barrel. This provides a potential floor on the price of oil if the plan is followed through, limiting potential downside in price.

Starting end of November, the administration followed its promise to wind down the use of the Strategic Petroleum Reserves. They drew just 1.4 million barrels in the week, far lower than the average of 6 million barrels/week over the past two months. However, this led to crude inventories in the country to plummet sharply by 12.79 million barrels. Still, this poses a potential challenge for the administration as it can no longer supplement crude supply in the country using Strategic Petroleum Reserves leading to higher demand in the open market.

US CRUDE INVENTORIES

Crude oil inventories in the US have seen large declines over the past three weeks. Contrasting this with Gasoline and Distillate stockpiles, which have instead increased. This is a result of high crack spread, which represents refining profit margins. As a result, US refineries are running at 93% of capacity highlighting that although crude oil stocks have been declining, it is primarily due to windfall margins available to refiners instead of high demand for crude oil.

G7-RUSSIA PRICE CAP

The EU has imposed an embargo on imports of Russian Crude Oil by sea using G7 and EU tankers.

G7, Australia, and 27 EU countries imposed a price cap on Russian crude oil transported by ship. The cap is aimed at reducing the margins that Russia makes on crude oil sales which it is alleged to fund its military actions in Ukraine. The price cap provides third countries the ability to acquire Russian Crude Oil at or below the price cap.

The price cap was set at $60 per barrel, while Russian Crude Oil closed at $67 per barrel on Friday. The level will be reviewed every two months, starting in mid-January, to make sure it stays at least 5% below the average price for Russian crude as determined by the IEA. Each change in the cap will be unanimously agreed by all 27 countries of the EU and then by the G7.

The price cap makes it challenging for Russia to sell its Crude Oil at a higher price as most shipping companies are based in the G7. This could provide a source of cheaper crude for countries that still trade with Russia, thereby lowering the demand for the more expensive WTI Crude oil.

Notably, Russia stated that it would not accept the price cap and would not sell its oil subject to the price cap, even if it is forced to curtail production. Additionally, Russia is already selling its Crude Oil at discounted rates to China and India relative to WTI or Brent.

TECHNICAL SIGNALS AND PEEK INTO COT REPORT

CME’s NYMEX WTI Crude Oil Futures (February 2023) closed at $77.37, below the Pivot Point $82.61 as on Tuesday. R1 from the pivot indicator was at $91.62 while S1 was at $71.48. CME’s NYMEX WTI Crude Oil futures hit a low of $73.6 on November 28 before rebounding.

Stochastic indicator was at neutral as on Monday while RSI recently intersected its declining SMA which could point to a potential reversal in the downtrend.

100-day moving average is currently declining and stands at $87.4757, in case the short-term moving average (10 days) intersects this, it could point to a potential breakout. 10-day MA is currently at $78.77. For now, the 100-day moving average acts as resistance.

According to the CME Commitment of Traders tool, we observe that Users, Managed Money, and Swap Dealer short positions declined between November 22 and November 29. Other reportable and non-reportable short positions went up. Long positions also declined by a similar margin while spread positions increased 3.3%.

ATM Implied Volatility from WTI Crude Oil options on CME was at 48.25% on Friday, down from ~53% in the prior week. This provides a daily expected move of 3.04%. As such the low on 28/November is within 1x standard deviation of the pivot support ($73.65) and 2x standard deviations of the pivot support is at $75.83.

TRADE SETUP

CME NYMEX Micro WTI Crude Futures provide exposure to 100 Barrels of WTI Crude oil with a maintenance margin of $750. This provides a cost-effective way to get exposure to movements in Crude’s price.

Short Position on CME NYMEX Micro WTI Crude Futures – February 2023 Contract

Entry: $77.80/barrel

Take Profit Target 1: $75.83/barrel

Take Profit Target 2: $73.65/barrel

Stop Loss: $82.61/barrel

Establishing a short position CME NYMEX Micro WTI Crude Futures (February) with an entry price at $77.80/barrel with a potential take profit target at $75.83/barrel by February could provide exposure to a short-term correction in the price of WTI crude yielding 26.27% returns or $197. A stop loss at the Pivot Point $82.61/barrel would protect against an unexpected rally resulting in loss of $481 or -64.13% providing a reward to risk ratio of 0.41. Alternatively, holding the position until 1x standard deviation of IV of ATM option above the pivot point would lead to 55.33% returns or $415 resulting in a reward-risk ratio of 0.86.

CME’s full-size NYMEX WTI futures provide exposure to 1,000 barrels of WTI crude with a maintenance margin of $7,300 at the time of writing and provide improved liquidity in case of larger positions.

MARKET DATA

CME Real-time Market Data help identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

DISCLAIMER

Trade ideas cited above are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management under the market scenarios being discussed. They shall not be construed as investment recommendations or advice. Nor are they used to promote any specific products, or services.

This material has been published for general education and circulation only. It does not offer or solicit to buy or sell and does not address specific investment or risk management objectives, financial situation, or particular needs of any person.

Advice should be sought from a financial advisor regarding the suitability of any investment or risk management product before investing or adopting any investment or hedging strategies. Past performance is not indicative of the future performance.

All examples used in this workshop are hypothetical and are used for explanation purposes only. Contents in this material is not investment advice and/or may or may not be the results of actual market experience.

Mint Finance does not endorse or shall not be liable for the content of information provided by third parties. Use of and/or reliance on such information is entirely at the reader’s own risk.

These materials are not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject Mint Finance to any registration or licensing requirement.

$FXI breakoutFXI is flirting with breaking out of the weekly downtrend here. over 29.46 I am long. huge buyer on 12/16 25 and 26 calls.

Looking For Some China PullbacksWhen it comes to China I like to watch the Hang Seng Index. That index remains in a bullish bias complexion with resistance levels at 19,706.90 and 19,983.24. Downside potential areas are 19,483.56, 19.260.22. China has been experiencing self-government policies, of which, are dictating their markets significantly. All-in-all, I do not correlate the two as relevant to overall market strength, sentiment, or complexion to the NYSE.

EUR/USD Technical AnalysisReversal trend has formed. Looking for pullback to enter long and confirmation of strong support level.

Need to hold 0.99 level in order to keep the bullish trend.

The 2023 trader playbook - the 5 biggest themes for the yearWith next week’s US CPI print and FOMC meeting offering the potential for further market volatility, it feels like these landmines are a fitting end to an incredibly eventful 2022.

We look back at the big themes that have driven cross-asset volatility and the conditions through which we’ve all had to adapt our trading – these include persistently high inflation, a worrying spike in the cost of living and aggressive rate hikes – yet resilient growth. We can also look at more regional-focused issues – a UK gilt tantrum driven by the Truss govt’s unfunded mini-budget, the invasion of Ukraine, the MOF/BoJ intervening to buy JPY and China’s Covid Zero policy.

The culmination of these factors created huge cross-asset volatility, decade-long market regime changes and lasting trending conditions.

Looking into 2023

Markets live in the future, and we look forward to the key themes that could cause volatility throughout 2023 – what’s important is not just to fully note these macro factors, but to understand the trigger points that offer a higher conviction of when to express the themes – taking this further, knowing the markets/instruments and strategies to express the theme is obviously advantageous.

These themes could alter market volatility, range expansion and market structure - so regardless of whether you’re purely automated or discretionary, it can pay to be aware.

While there are many more, these are five potential themes that I am looking at closely for 2023 that if triggered would affect the markets we trade.

1 - High inflation worries morph into growth concerns and a higher probability of a recession

US and global inflation in decline

• Market pricing (i.e. the inflation ‘fixings’ market) of future inflation shows US CPI inflation expected to fall to around 3% by year-end

• US M2 money supply has fallen from 26% to 1.3% - US headline CPI typically lags by 16 months

• Manufacturing PMI delivery-lead times and supply chain data suggest inflation falls hard in 2023

• Unit labour costs falling to 2.1%

Growth – while the consensus from economists is that the US economy narrowly avoids a recession, and EPS expectations have not been revised down to reflect recessionary conditions - the markets see a higher probability of this outcome – I back the markets, where we see:

• All parts of the US yield curve are inverted – US 2s vs 10s are the most inverted since 1981

• The US leading index (measures 10 key economic indicators) has turned negative and falling fast – this has an exemplary record of predicting US recessions

• Comments from the CEOs of Goldman Sachs and BoA warning of tougher times ahead

Themes to trade as we price in a recession

• Consensus EPS expectations are cut by around 20% (from the highs), in turn, lifting PE multiples – traders will assess the trade-off between earnings downgrades vs a lower discount rate

• Steeper yield curves are a trigger – while now is not the time to put on curve steepeners, when short-dated US Treasury bond yields do fall/outperform, we’ll see a steeper yield curve – this could be the trigger for a sharp equity rally, led by financials

• As the US data deteriorates, we will likely see equity market drawdown, US treasury buying and selling of risk FX - it’s when central bankers acknowledge that growth is a greater concern the market will feel validated in its pricing of rate cuts – it’s here we see a risk rebound, broad USD selling and housing + lumber outperforming

• As bond yields fall, we should see solid outperformance from the JPY and CHF and EM assets

• USD initially works selectively vs global FX, but then reverses as conviction of the Fed cutting impacts and traders look ahead to a trough in the global growth slowdown

• Gold and silver rally hard as a hedge vs recession risk

2 - Central bank policy – assessing the potential for rate cuts

• The base case is rate hikes finish in Q1 23, followed by a pause – we then explore the possibility of rate cuts through Q4 23 – the Fed are clearly data dependent, so trends in the US (and global) data through Q2 will be key to markets

• Since 1995 there have been five occasions when the Fed has moved from hikes to rate cuts – the average time it takes to play out is 10.6 months (the longest period being 18 months, the shortest being 5 months)

• G7 balance sheet reduction and liquidity drain - Quantitative Tightening (QT) is a big unknown. Federal Reserve liabilities are expected to fall towards $2.5t, a level where the market is concerned about the scarcity of reserves – traders will start to pay attention to the Fed funds effective – interest earned on excess reserves (IOER) spread for signs of scarcity and concerns that the repo market may be impacted and need support.

• It’s not just the Fed but the ECB and BoE (and others) will be reducing their balance sheets.

3 - China reopening and China's market outperformance

We’ve already seen a plethora of measures announced and Chinese markets have rallied hard – China is the elephant in the room when it comes to the global growth outlook for 2023 – a weak 1H23 seems likely but this will then followed by far stronger growth in 2H23 – after a poor 2022, Chinese assets could really outperform in 2023

• Long HK50 / short NAS100 could be a trade to look at if markets de-risk on a higher probability of a US recession

4 - BoJ policy recalibration – time for the JPY to fly

BoJ chief Kuroda steps down in April but there are already plans for a review of BoJ policy – it feels inevitable that we’ll see a 25bp lift to the BoJ’s YCC target to 50bp – we’ve already seen signs that Japanese banks/pension funds are moving capital back to Japan to get a more compelling return in the JGB market – but could a major policy change cause tremors in global bond markets and promote significant inflows into the JPY?

5 - Politics & Geopolitics – great for volatility, bad for humanity

Obviously one of the most important issues in 2022, not just for markets but humanity - always a hard one for traders to price risk around

• China/Taiwan – unlikely to be a 2023 story (hopefully not at all) but one that will come into the headlines periodically

• US and European/China relations

• Russia/Ukraine – could we hear more constructive signs of a ceasefire?

• Russia vs NATO – Putin has already suggested that the risk of a nuclear war has been rising – obviously if this really escalates it has the premise to dominate markets

• Given the divided Congress, could we see the US debt ceiling become a market concern?

Good luck to all

Silver is outperforming Apple as global trust declinesCommodities are hard assets and are trustless. The geo political climate has made commerce more difficult. Russia conflict, China supply issues, USA raising the cost of funding, the world is de-globalizing at the moment. Silver is tangible, credit is a promise that requires trust. As credit and trust are stalling temporarily, businesses will find it difficult to grow.

Alibaba - China beneficiary Alibaba - Short Term - We look to Buy at 87.66 (stop at 79.09)

Broken out of the wedge formation to the upside. Broken out of the Head and Shoulders formation to the upside. Neckline support is 85.91. The formation has a measured move target of 113.48. Further upside is expected although we prefer to set longs at our bespoke support levels at 87.66, resulting in improved risk/reward.

Our profit targets will be 113.48 and 120.70

Resistance: 94.84 / 104.85 / 120.70

Support: 87.60 / 79.86 / 75.88

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Signal Centre’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Signal Centre.

HSI/SPY - time to be aware of ChinaKeep in mind this is a monthly chart, so we're looking at years and decades here.

This ratio chart of the HANG SENG INDEX divided by SPY is warning of a coming rush by investors into the Chinese markets. The China C wave I posted about may be done (see post attached below). If this falling wedge breaks out we could see a monumental shift towards the Chinese markets in the coming years, possibly spurred by their willingness to relax Covid controls and/or get better vaccines. This is a market mostly ignored by retail investors and that may change soon.

The monthly RSI has sharp bullish divergence. The monthly 18ma is sitting at 51.3 as I type today, getting over and holding that on a monthly close would be very bullish for HSI.

Good luck!

CHINA MOMENT OF DECISIONMajor 30 year bull trend line seems to be respected.

Though... many lines crosses here as well. It is a very narrow band with to, each now either up BIG, or down BIG.

All other chines indices indicate somehow the same for BIG up or BIG down.

Im at the short side... Will see what happens here.

BIG long SuningSuning already got a 6 years bottom.

That means it's will group up (possible) until the past 3 year's middle price.

AUDUSD Bullish setup after positive China news and a weak DollarThis looks like a nice setup to the upside. We're seeing a weak dollar and expecting some bullish pressure after positive developments in China.

CN1!HELLO GUYS THIS MY IDEA 💡ABOUT CN1! is nice to see strong volume area....

Where is lot of contract accumulated..

I thing that the sellers from this area will be defend this SHORT position..

and when the price come back to this area, strong sellers will be push down the market again..

DOWNTREND + SUPPORT from the past + Strong volume area is my mainly reason for this short trade..

IF you like my work please like and follow thanks